|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

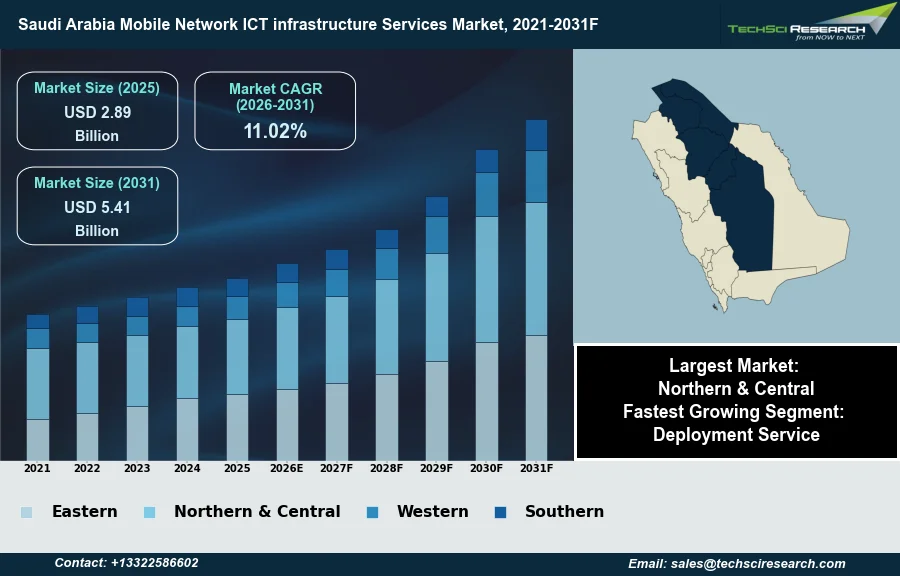

Market Size (2025)

|

USD 2.89 Billion

|

|

CAGR (2026-2031)

|

11.02%

|

|

Fastest Growing Segment

|

Deployment Service

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 5.41 Billion

|

Market Overview

The Saudi Arabia Mobile Network ICT infrastructure Services Market will grow from USD 2.89 Billion in 2025 to USD 5.41 Billion by 2031 at a 11.02% CAGR. The Saudi Arabia Mobile Network ICT Infrastructure Services Market encompasses the provision, deployment, maintenance, and upgrade of essential hardware, software, and associated services for mobile telecommunication networks within the Kingdom. This includes cellular base stations, core network elements, transmission systems, network management solutions, and professional services supporting network planning, optimization, and security. Market growth is primarily driven by ambitious digital transformation initiatives, notably Saudi Vision 2030, which fosters a knowledge-based digital economy. Expanding data consumption, fueled by increased online activities, alongside accelerated 5G network deployment, further propels market expansion by enabling new applications like the Internet of Things (IoT) and smart cities.

A significant challenge impeding market expansion is the substantial capital expenditure required for continuous network upgrades, including 5G buildout and fiber deployment, to meet evolving technological demands and maintain competitiveness. According to the GSMA, in November 2025, Saudi Arabia demonstrated global leadership in IoT adoption, with an anticipated return-on-investment period of merely 3.3 years, signaling sustained demand for advanced infrastructure to support such initiatives.

Key Market Drivers

Vision 2030 catalyzes ICT infrastructure investment

Vision 2030 and its accompanying digital transformation initiatives are primary catalysts for the Saudi Arabia Mobile Network ICT Infrastructure Services Market. These national programs aim to diversify the economy and build a robust, knowledge-based digital society, necessitating substantial investment in advanced communication infrastructure. This strategic direction fuels demand for network planning, deployment, optimization, and maintenance services. For instance, in July 2025, STC secured a SAR 32.64 billion contract with a government entity to design, build, and manage telecom infrastructure over the next 15 years, directly supporting the Kingdom's digital aspirations. This commitment underpins the government-backed impetus to enhance the nation's digital backbone.

5G expansion drives ICT infrastructure demand

Extensive 5G network deployment and ongoing expansion further drive the market for mobile network ICT infrastructure services. As demand for high-speed, low-latency connectivity grows, telecommunication operators invest heavily in upgrading and extending their 5G networks, including core network elements and transmission systems. This requires significant capital expenditure for new base stations and advanced antenna technologies. A notable example is Zain KSA, which invested USD 357 million in CAPEX during 2025 to expand its 5G coverage across 66 cities. These investments are critical for supporting surging data consumption and enabling emerging technologies. The broader Saudi Arabia ICT sector was valued at nearly $48 billion as of May 2025, accounting for over 4 percent of the Kingdom's GDP.

Download Free Sample Report

Key Market Challenges

Capital Expenditure for 5G and Fiber Upgrades

A significant challenge impeding the growth of the Saudi Arabia Mobile Network ICT Infrastructure Services Market is the substantial capital expenditure required for continuous network upgrades and expansion. This includes investments in the latest technologies, such as 5G buildout and advanced fiber deployment, which are essential for meeting evolving technological demands and maintaining a competitive edge within the rapidly advancing digital economy. The high financial outlay for these complex infrastructure projects places considerable pressure on mobile network operators.

Ongoing Investment Burden and Spectrum Payment Obligations

The need for continuous and extensive investment directly hampers market expansion by increasing the financial burden on operators, potentially slowing down the pace of infrastructure development. According to the GSMA, in December 2024, mobile network operators in Saudi Arabia expressed concerns about the significant investments necessary to fulfill stringent coverage and quality of service obligations, particularly across low-population density regions. This includes ongoing financial commitments for newly acquired spectrum bands, with annual payments for various bands initiating in July 2025 and for the 600 MHz band starting in July 2026. Such substantial and recurrent expenditures can limit operators' capacity to innovate rapidly or extend services to areas with lower immediate return on investment.

Key Market Trends

Fiber backhaul expansion and network densification in Saudi Arabia

The increasing demand for high-capacity, low-latency connectivity is driving significant growth in fiber optic backhaul and network densification across Saudi Arabia. Operators are investing in expanding their fixed-line infrastructure to support the proliferation of mobile data, Internet of Things devices, and upcoming smart city initiatives. This trend involves not only laying new fiber cables but also upgrading existing networks to higher capacities and densifying coverage, particularly in urban and underserved areas, to ensure robust and resilient connectivity. According to The Saudi Standard, July 2025, in the 'Rawasi Al-Bina Secures STC Deal for Fiber Network Rollout' article, Rawasi Al-Bina Investment Company signed a five-year framework agreement with STC for external fiber optic network rollout, with the financial impact expected to exceed 5% of Rawasi's 2024 revenue. This expansion is crucial for enhancing the overall network backbone and ensuring seamless service delivery.

Shift to cloud-native networks enabling agile 5G and cloud services

Another pivotal trend shaping the market is the transition towards cloud-native network architectures, moving away from traditional hardware-centric infrastructure. This shift enables greater network agility, scalability, and efficiency through software-defined networking and virtualization of core network functions. By leveraging cloud platforms, operators can rapidly deploy new services, manage resources dynamically, and reduce operational expenditures, aligning with the evolving demands of 5G Standalone networks and advanced digital services. According to Saudi 5G and Telecommunications, May 2026, the center3-HUMAIN joint venture announced in late 2025 committed to up to 1 GW of AI data center capacity in Saudi Arabia, with the initial 250 MW phase already in design, supporting the foundational infrastructure for such cloud-based transitions. This architectural evolution is fundamental to unlocking the full potential of next-generation mobile communication.

Segmental Insights

Deployment Services Growth Fueled by Vision 2030, 5G Modernization, and CST Regulation

The Deployment Service segment is experiencing rapid growth within the Saudi Arabia Mobile Network ICT infrastructure Services Market, driven by the Kingdom's ambitious digital transformation initiatives under Vision 2030. This expansion is fueled by the accelerated deployment and widespread modernization of 5G networks across urban centers and giga-projects, demanding significant infrastructure implementation. Furthermore, increasing enterprise digitalization and the development of smart cities necessitate extensive new network installations. The Communications, Space and Technology Commission (CST), as the primary regulatory body, plays a crucial role in enabling these investments and fostering a competitive environment for infrastructure development.

Regional Insights

Northern and Central Region Leads the Saudi Mobile Network ICT Infrastructure Market

The Northern and Central region stands as the principal contributor to the Saudi Arabia Mobile Network ICT infrastructure Services Market. This dominance stems from Riyadh's pivotal role as the nation's capital, economic, and administrative center. The region experiences significant urbanization and a high demand for advanced digital services, driving extensive investments in cutting-edge infrastructure, particularly 5G network deployments. Government initiatives supporting smart city developments in Riyadh further accelerate telecommunications investments. The concentration of federal government entities, major financial institutions, and multinational corporate headquarters within this region inherently generates substantial demand for sophisticated ICT services. This robust environment, fostered in part by the Communications, Space and Technology Commission, positions Northern and Central as the undisputed leader in the market.

Recent Developments

-

In March 2025, Nokia and Zain KSA successfully completed Saudi Arabia's first live Cloud RAN (Radio Access Network) site. The trial, conducted between December 2024 and January 2025, utilized Nokia's 5G anyRAN solution and achieved high download speeds. This milestone demonstrates the advantages of cloud-native architectures, including improved efficiency, reduced total cost of ownership, and faster deployment times. This deployment supports the scaling of networks and the development of new digital applications for communications service providers and enterprise customers, reinforcing Saudi Arabia's leadership in 5G innovation within its mobile network ICT infrastructure services market.

-

In July 2024, stc Group and Ericsson achieved a significant milestone by deploying the world's first Automated Radio Resource Partitioning on a 5G standalone network slice in a live environment. This breakthrough research leverages intent-based automation to optimize the dynamic allocation of network resources, enhancing efficiency and user experience. The advanced software feature is part of Ericsson's 5G Advanced offerings, enabling stc Group to prepare for future 5G Advanced capabilities. This development underscores a commitment to pioneering advancements in the telecommunications industry within Saudi Arabia's mobile network ICT infrastructure.

-

In April 2024, the Public Investment Fund (PIF) and stc Group announced definitive agreements to merge Telecommunication Towers Company (TAWAL) and Golden Lattice Investment Company (GLIC), forming the region's largest telecom tower entity. The PIF acquired a 51% stake in TAWAL from stc Group, with the combined new entity expected to be owned 54% by PIF and 43.1% by stc Group. This consolidation aims to enhance consumer experience and network coverage, as well as improve connectivity and mobile internet speeds by unifying Saudi Arabia's tower assets. The transaction, expected to be completed in the second half of 2024, aligns with strengthening the country's mobile network ICT infrastructure.

-

In January 2024, Aramco Digital and Intel announced their intention to establish Saudi Arabia's first Open RAN (Radio Access Network) Development Center. This collaboration is designed to foster innovation, drive technological advancements, and contribute significantly to the Kingdom's digital transformation. The center aims to accelerate the development and deployment of Open RAN technologies, thereby enabling Saudi Arabia to build a robust and agile telecommunications infrastructure. This initiative supports the broader national goal of accelerating digitalization across various industries, aligning with Saudi Arabia's Vision 2030 objectives for technological progress and economic diversification within the mobile network ICT infrastructure services market.

Key Market Players

- Ericsson

- Nokia

- Huawei

- Samsung

- ZTE

- STC

- Mobily

- Zain

- Al Futtaim Telecom

|

By Service Type

|

By Deployment Mode

|

By End User

|

By Region

|

- Deployment Service

- Professional Service

- Managed Service

- Maintenance Service

- Neutral Hosting Service

|

|

- Mobile Network

- Service Vendor

- Enterprise

- Government

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Mobile Network ICT infrastructure Services Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Mobile Network ICT infrastructure Services Market, By Service Type:

-

Deployment Service

-

Professional Service

-

Managed Service

-

Maintenance Service

-

Neutral Hosting Service

-

Saudi Arabia Mobile Network ICT infrastructure Services Market, By Deployment Mode:

-

Saudi Arabia Mobile Network ICT infrastructure Services Market, By End User:

-

Mobile Network

-

Service Vendor

-

Enterprise

-

Government

-

Others

-

Saudi Arabia Mobile Network ICT infrastructure Services Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Mobile Network ICT infrastructure Services Market.

Available Customizations:

Saudi Arabia Mobile Network ICT infrastructure Services Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Mobile Network ICT infrastructure Services Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com