|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

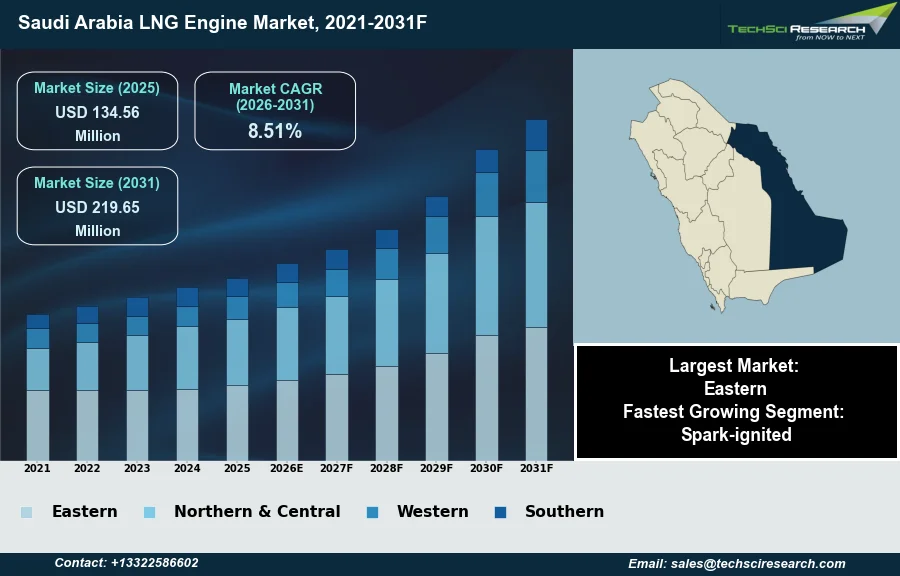

Market Size (2025)

|

USD 134.56 Million

|

|

CAGR (2026-2031)

|

8.51%

|

|

Fastest Growing Segment

|

Spark-ignited

|

|

Largest Market

|

Eastern

|

|

Market Size (2031)

|

USD 219.65 Million

|

Market Overview

The Saudi Arabia LNG Engine Market will grow from USD 134.56 Million in 2025 to USD 219.65 Million by 2031 at a 8.51% CAGR. Liquefied natural gas (LNG) engines utilize natural gas, cooled to a liquid state, as a primary fuel source, offering a cleaner combustion alternative to conventional diesel in various industrial, marine, and heavy-duty transport applications. The market for these engines in Saudi Arabia is significantly driven by the Kingdom's Vision 2030, which mandates economic diversification and a robust commitment to environmental sustainability through reduced carbon emissions. These national strategic imperatives encourage the adoption of cleaner energy solutions across critical sectors, including a growing emphasis on transportation and power generation. According to Saudi Aramco, its natural gas production reached 11.1 billion cubic feet per day in the first half of 2025, demonstrating an expanding domestic gas supply that underpins the availability of LNG for engine applications.

Further supporting market growth is the ongoing strategic expansion of LNG infrastructure and supply networks, with Saudi Aramco targeting a long-term LNG portfolio of 20 million tons per year. Despite these favorable drivers, a notable challenge impeding market expansion is the substantial initial capital expenditure associated with establishing the necessary LNG refueling and distribution infrastructure, which can present a significant financial barrier for widespread adoption across diverse end-use sectors.

Key Market Drivers

Vision 2030-Driven Diversification Boosts LNG Engine Demand

The Saudi Arabia LNG Engine Market is significantly propelled by the Kingdom's Government-Led Energy Diversification Initiatives under Vision 2030, which prioritizes a shift towards cleaner energy sources and economic sustainability. These strategic directives foster an environment conducive to adopting natural gas as a primary fuel in various sectors. This commitment is evident in substantial investments in renewable energy projects to complement the gas transition; for example, according to The Energy Year, in December 2025, ACWA Power and its partners achieved financial close on seven solar and wind projects in Saudi Arabia, representing a combined investment of USD 8.2 billion. This diversification strategy directly drives the demand for LNG engines, as sectors aim to align with national environmental and economic objectives by reducing reliance on traditional liquid fuels.

Expanding LNG Infrastructure and Domestic Gas Supply

Further boosting the market is the expanding LNG Infrastructure and Domestic Gas Production, which ensures a reliable and increasing supply of liquefied natural gas. The development of major gas fields and processing facilities is crucial for making LNG readily available for engine applications across the industrial, marine, and transportation sectors. A significant milestone in this expansion was achieved when, according to World Oil, in December 2025, Aramco commenced initial production from the Jafurah unconventional gas field, with phase-one facilities now producing 450 million standard cubic feet per day. This enhanced domestic supply is fundamental to supporting the transition away from liquid fuels. The overall market is set to benefit as Saudi Aramco aims to replace up to 500,000 barrels per day of crude oil currently used for domestic power generation with gas by 2030, according to CompressorTech2.

Download Free Sample Report

Key Market Challenges

Upfront capital barriers for LNG refueling and distribution infrastructure

The substantial initial capital expenditure required for establishing the necessary LNG refueling and distribution infrastructure presents a significant impediment to the growth of the Saudi Arabia LNG engine market. Developing new networks demands considerable upfront investment in cryogenic storage facilities, specialized transport vehicles, and sophisticated dispensing units. This high capital intensiveness creates a notable financial barrier, particularly for businesses, especially smaller entities, contemplating a transition to LNG-powered industrial machinery and heavy-duty vehicles.

Protracted payback and funding hurdles for LNG adoption

The extended payback periods associated with these large investments make LNG engine adoption less appealing compared to established conventional fuel options, despite their cleaner combustion benefits and long-term operational cost savings. According to the International Energy Agency (IEA), the Middle East region is projected to invest approximately USD 130 billion in oil and gas supply during 2025, underscoring the substantial financial scale of energy infrastructure development. This immense capital requirement for broader gas infrastructure highlights the specific challenge faced by the nascent LNG engine market in securing dedicated funding for its unique distribution and refueling needs, thereby slowing widespread market penetration and accessibility across various end-use sectors.

Key Market Trends

Rising LNG-Powered Maritime Propulsion and Marine-Engine Demand

The Saudi Arabia LNG Engine Market is significantly influenced by the rising deployment of LNG for propulsion in marine vessels. This trend is driven by increasing environmental regulations in the maritime sector and the economic benefits of LNG as a cleaner fuel alternative, encouraging vessel operators to transition away from conventional marine fuels. A notable instance of this trend was observed when PIL's LNG-powered Kota Odyssey made its maiden call at a Saudi Arabian port, the Red Sea Gateway Terminal, in February 2026, marking its entry into the Red Sea region. This event highlights the growing acceptance and operational integration of LNG-fueled ships within Saudi Arabia's maritime domain, stimulating demand for marine-specific LNG engine technologies and related bunkering services in the Kingdom.

Expansion of Industrial and Off-Grid LNG Applications

Concurrently, the increasing utilization of LNG for industrial and off-grid power generation represents another pivotal trend. Industries and remote operations are progressively adopting LNG engines as a reliable and cleaner source for electricity, reducing reliance on diesel generators and aligning with broader environmental objectives. This shift is exemplified by GE Vernova's announcement in November 2025 regarding the start of commercial operations at the Jafurah Cogeneration Independent Steam and Power Plant, which features the company's first H-Class gas turbine completed in Saudi Arabia. This development underscores a strategic move towards cleaner energy solutions for industrial processes and off-grid energy needs, thereby expanding the application scope and market for LNG engines in various industrial sectors across Saudi Arabia.

Segmental Insights

Spark-ignited LNG growth driven by Vision 2030 and SASO support

The Spark-ignited segment is experiencing rapid growth in the Saudi Arabia LNG Engine Market, primarily driven by the Kingdom's strategic commitment to energy diversification and environmental sustainability under Vision 2030. This expansion is bolstered by significant regulatory support, including initiatives from the Saudi Standards, Metrology and Quality Organization (SASO), which actively promotes the adoption of cleaner energy solutions. Spark-ignited LNG engines are increasingly favored for their operational efficiency and their capability to achieve demanding emission reduction targets, presenting a compelling and environmentally conscious alternative to traditional fossil fuels across key sectors such as industrial applications, marine, and transportation. This aligns with national efforts to mitigate air pollution and greenhouse gas emissions, reflecting a broader shift towards a more sustainable energy landscape.

Regional Insights

Eastern Province: Market Leader Fueled by Industrial Base, Gas Infrastructure, and Vision 2030

The Eastern Province dominates the Saudi Arabia LNG Engine Market due to its established position as the Kingdom's primary industrial and economic hub. This region features a high concentration of industrial activities, power generation facilities, and crucial maritime infrastructure, driving substantial demand for LNG engines across various applications. Proximity to abundant natural gas reserves and a robust gas processing network, largely managed by Saudi Aramco and its Master Gas System, ensures reliable LNG supply. Furthermore, the Eastern Province's strategic alignment with national economic diversification objectives and initiatives to adopt cleaner energy solutions, such as those under Vision 2030, reinforces its leadership in the market.

Recent Developments

-

In November 2025, GE Vernova announced the start of commercial operations for its first H-Class gas turbine completed in Saudi Arabia, situated at the Jafurah Cogeneration Independent Steam and Power Plant. This deployment was a key component of the Jafurah unconventional gas field development, a strategic project by Saudi Aramco. The advanced gas turbine technology directly supports Saudi Arabia's objective to displace liquid fuels in power generation with natural gas. This significant new product launch and project milestone demonstrated technological progress in large-scale gas-fired power solutions, thereby expanding the potential for sophisticated natural gas engine applications within the Saudi Arabia LNG Engine Market.

-

In May 2025, ACWA Power engaged in a partnership with GE Vernova focused on testing and implementing innovations for core equipment in combined-cycle gas turbine projects within Saudi Arabia. This collaboration extended to advancements in electricity transmission and distribution systems across the Kingdom. The agreement aimed to leverage expertise to enhance the performance and efficiency of gas turbine technologies used in power generation. Such initiatives represent a direct company collaboration and contribute to breakthrough research by developing and integrating advanced gas engine solutions, thereby supporting technological evolution and adoption within the stationary power segment of the Saudi Arabia LNG Engine Market.

-

In September 2024, Saudi Arabia officially commenced operations at the Hawiyah Gas Storage facility, developed by Aramco, marking the Kingdom's inaugural project for storing natural gas through processed fuel injection. This significant infrastructure launch aimed to reintroduce up to 2 billion standard cubic feet of natural gas per day into Saudi Arabia's Master Gas System. The initiative was designed to address rising domestic energy demand, particularly during peak periods, and to support the Liquid Fuel Displacement Program. By enhancing the reliable supply of natural gas, this project directly facilitated the wider adoption and operational viability of LNG engines within the power generation and industrial sectors across the Saudi Arabia LNG Engine Market.

-

In June 2024, Aramco advanced its strategy to become a prominent global LNG player by entering into significant non-binding agreements for LNG supply. The company signed a deal with Sempra for five million tonnes per annum of liquefied natural gas from the Port Arthur LNG Phase 2 expansion project for a 20-year term, including potential equity participation. Simultaneously, an initial agreement was reached with NextDecade for the purchase of 1.2 million tonnes per annum of LNG from its Rio Grande LNG export project. These collaborations, aimed at securing long-term LNG volumes, were crucial for strengthening Aramco's gas portfolio and underpinning the foundational supply necessary for the growth of the Saudi Arabia LNG Engine Market.

Key Market Players

- Caterpillar

- MAN Energy Solutions

- Wärtsilä

- GE Power

- Rolls-Royce

- Al Futtaim LNG

- Al Naboodah LNG

- Local Energy Suppliers

- Aramco Partners

|

By Type

|

By End Use

|

By Region

|

- Spark-ignited

- Diesel-ignited

- Direct Gas Injection

|

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia LNG Engine Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia LNG Engine Market, By Type:

-

Spark-ignited

-

Diesel-ignited

-

Direct Gas Injection

-

Saudi Arabia LNG Engine Market, By End Use:

-

Saudi Arabia LNG Engine Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia LNG Engine Market.

Available Customizations:

Saudi Arabia LNG Engine Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia LNG Engine Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com