|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

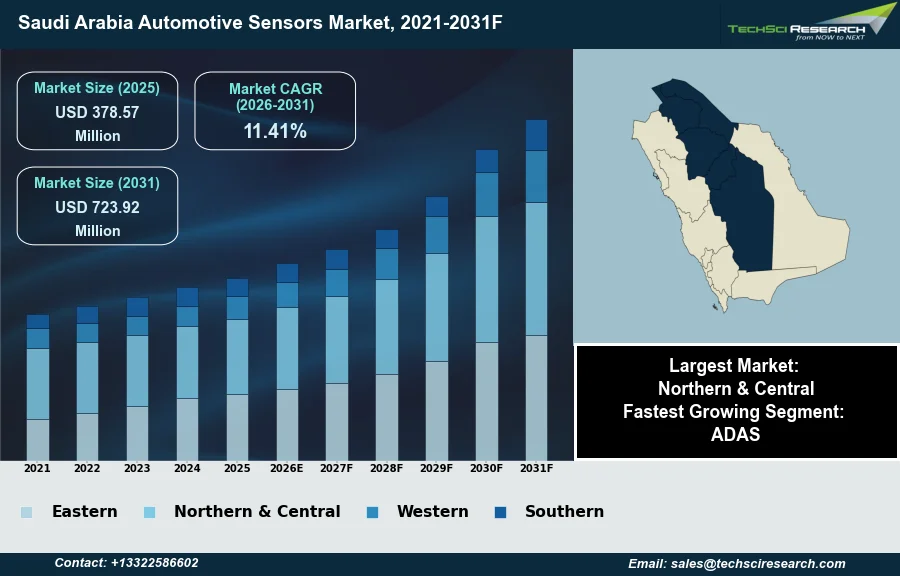

Market Size (2025)

|

USD 378.57 Million

|

|

CAGR (2026-2031)

|

11.41%

|

|

Fastest Growing Segment

|

ADAS

|

|

Largest Market

|

Northern & Central

|

|

Market Size (2031)

|

USD 723.92 Million

|

Market Overview

The Saudi Arabia Automotive Sensors Market will grow from USD 378.57 Million in 2025 to USD 723.92 Million by 2031 at a 11.41% CAGR. Automotive sensors are electronic components designed to detect and measure physical quantities such as temperature, pressure, speed, and position within a vehicle, converting these into electrical signals for vehicle control systems. The Saudi Arabia automotive sensors market growth is predominantly driven by increasing government mandates for vehicle safety features, the accelerating integration of advanced driver-assistance systems (ADAS) in new vehicle models, and a burgeoning domestic automotive manufacturing sector. These factors collectively enhance the demand for sophisticated sensor technologies to improve both vehicle performance and passenger safety.

The expansion of the automotive market provides a substantial foundation for sensor demand. According to the International Organization of Motor Vehicle Manufacturers, in 2025, new vehicle sales in Saudi Arabia reached 827,544 units. However, a notable challenge impeding market expansion is the scarcity of adequately trained technicians capable of servicing and calibrating complex sensor systems, leading to potential maintenance and repair complexities within the aftermarket.

Key Market Drivers

ADAS Adoption and Safety Initiatives Drive Saudi Automotive Sensors Market

The increasing emphasis on vehicle safety and the accelerating integration of Advanced Driver-Assistance Systems (ADAS) significantly drives the Saudi Arabia automotive sensors market. Government initiatives and evolving consumer expectations for safer vehicles propel demand for sensor technologies like radar, lidar, and ultrasonic sensors, fundamental to ADAS functions such as adaptive cruise control, lane keeping assist, and automatic emergency braking. These systems rely on an array of sophisticated sensors to perceive surroundings and mitigate accident risks. The Kingdom's commitment to enhancing its transportation infrastructure further supports this trend; according to WifiTalents, in February 2026, $30 billion is allocated for road projects under Vision 2030, which creates a foundational environment for advanced safety features.

EV Adoption and Imports Elevate Sensor Demand in Saudi Arabia

The growing adoption of electric and hybrid vehicles (EVs and HEVs) is another critical factor influencing the market. These vehicles typically incorporate a higher number of sensors than conventional vehicles, necessitated by battery management systems, power electronics, and regenerative braking. Sensors are essential for monitoring battery temperature, state of charge, motor control, and overall system efficiency. This electrification shift aligns with global sustainability goals and Saudi Arabia's Vision 2030. According to Arab News, in May 2026, citing the International Energy Agency, EV sales in the Middle East reached around 75,000 units in 2025, with Saudi Arabia and Qatar accounting for approximately 45 percent of this regional demand. Additionally, according to Al-Arabiya.net, in June 2026, citing the Saudi Zakat, Tax and Customs Authority, vehicle imports to Saudi Arabia reached around 959,403 units by 2025.

Download Free Sample Report

Key Market Challenges

Shortage of Trained Technicians Hinders Market Expansion

The scarcity of adequately trained technicians presents a significant impediment to the expansion of the Saudi Arabia automotive sensors market. Modern automotive sensor systems, particularly those integrated into advanced driver-assistance systems, demand specialized expertise for accurate diagnosis, servicing, and calibration. A limited availability of professionals with the requisite skills directly translates into increased complexities and potential delays for vehicle maintenance and repair within the aftermarket.

Repair Capacity Constraints Affect Sensor Adoption

These maintenance and repair challenges can diminish consumer confidence in the reliability and serviceability of vehicles incorporating sophisticated sensor technologies. This directly impacts the adoption of new vehicles featuring advanced sensors and constrains the demand for replacement sensors. According to the Saudi Standards, Metrology and Quality Organization (SASO), approximately 30% of repair shops struggle to meet established requirements, indicating a substantial gap in the capabilities needed for complex systems. Furthermore, SASO reported that the total number of authorized vehicle maintenance and repair centers reached 585 in the first half of 2024, illustrating the concentrated nature of specialized service infrastructure. This limited capacity for expert servicing hinders the overall growth trajectory of the automotive sensors market.

Key Market Trends

Smart city infrastructure and mobility initiatives driving automotive sensor demand

The development of smart city infrastructure and innovative mobility solutions represents a significant trend influencing the Saudi Arabia automotive sensors market. As the Kingdom invests in advanced urban environments, there is an increasing demand for sensors that enable vehicle-to-everything communication, intelligent traffic management, smart parking systems, and autonomous public transport. These initiatives create a foundation for a sophisticated ecosystem where vehicles are integral components of a larger connected network, necessitating various environmental, proximity, and communication sensors. According to the Public Investment Fund Governor, April 2026, the PIF's companies attracted approximately SAR57 billion in direct foreign investment between 2021 and Q3 2025 across emerging sectors including transportation, logistics, and telecommunications and technology, underpinning the broader technological advancements supporting such smart mobility initiatives.

Localization of automotive production driving local sensor demand

Another pivotal trend is the growing localization initiatives for automotive production within Saudi Arabia. The establishment of domestic vehicle manufacturing facilities directly stimulates demand for locally sourced automotive sensors and related component technologies. This shift reduces reliance on imports and fosters a robust in-country supply chain capable of meeting specific design and functional requirements for vehicles assembled within the Kingdom. For instance, according to Logistics Middle East, June 2026, Lucid's AMP-2 plant, the Kingdom's first car factory, is expected to scale its capacity to approximately 150,000 EVs annually as it moves toward its 2026 production milestone, thereby creating substantial demand for a wide array of specialized sensors for these locally produced vehicles.

Segmental Insights

Regulatory Push and Market Demand Drive ADAS Growth

The Advanced Driver Assistance Systems (ADAS) segment is the fastest-growing component within the Saudi Arabia Automotive Sensors Market. This rapid expansion is primarily driven by the Kingdom's strong emphasis on enhancing road safety, a key objective under Saudi Vision 2030, which seeks to reduce traffic accidents and fatalities. Government initiatives and evolving regulatory frameworks, overseen by bodies like the Saudi Standards, Metrology and Quality Organization (SASO), promote the adoption of advanced safety features in vehicles. Furthermore, increasing consumer awareness and demand for enhanced vehicle safety, particularly within the luxury vehicle segment, are compelling manufacturers to integrate more ADAS technologies, such as collision avoidance and lane departure warning systems.

Regional Insights

Regional drivers of automotive sensors demand in Northern & Central Saudi Arabia

Northern & Central Saudi Arabia leads the automotive sensors market primarily due to its strategic economic importance and significant concentration of key industries. This region encompasses Riyadh, the capital and economic hub, which drives substantial demand for passenger and commercial vehicles equipped with advanced sensor technologies. The dominance is further supported by high population density, rising urbanization, and robust infrastructure, including extensive road networks. Additionally, government initiatives like Vision 2030 promote economic diversification and technological innovation, fostering increased investments in the automotive sector, including smart city projects and advanced mobility solutions predominantly focused in these areas, thereby boosting the demand for automotive sensors.

Recent Developments

-

In February 2025, Elitek Vehicle Services, an LKQ company, introduced its ADAS MAP (Advanced Driver Assistance Systems Mapping) solution. Powered by OPUS IVS technology, this software tool was designed to provide automotive repair shops with the necessary capabilities to accurately diagnose, calibrate, and repair advanced driver-assistance systems in vehicles. The solution aimed to enhance vehicle safety and service efficiency by ensuring proper functioning of ADAS components, which are intrinsically linked to various automotive sensors. This development supports the upkeep and reliability of sensor-based safety features in the Saudi Arabia automotive market.

-

In July 2024, Najm for Insurance Services Company, based in Saudi Arabia, launched a new telematics initiative to enhance road safety across the Kingdom. This program, a collaboration with Cambridge Mobile Telematics (CMT) and AiGeNiX, utilized advanced mobility analytics technologies. The initiative involved installing smart devices in vehicles to measure driving behavior, including speed, acceleration, braking, and adherence to traffic regulations. By analyzing data from these sensors, the system provided insights to evaluate driver risk levels, encouraging safer driving practices and directly impacting the application of automotive sensors for telematics in Saudi Arabia.

-

In March 2024, OMNIVISION announced that its OX08D10 8-megapixel (MP) CMOS image sensor, featuring new TheiaCel™ technology, achieved compatibility with Qualcomm Technologies' Snapdragon Digital Chassis™ platforms. This integration aimed at next-generation advanced driver assistance systems (ADAS) and artificial intelligence-enabled connected digital cockpits. The sensor offered enhanced capabilities such as superior high dynamic range (HDR), improved LED flicker mitigation, and better low-light performance. This breakthrough research and collaboration provided critical sensor technology for advanced automotive applications, relevant to the evolving automotive sensors market in Saudi Arabia as it adopts more sophisticated vehicle systems.

-

The search for OmniVision yielded direct press releases from Business Wire and PR Newswire (OmniVision's own announcement), as well as articles from Automotive Technology Insight and Sensing. This is a good, solid fourth news item. While the articles don't explicitly mention Saudi Arabia, the technology (ADAS and digital cockpits) is universally applicable to advanced automotive markets and aligns with Saudi Arabia's Vision 2030 goals for smart mobility and advanced automotive technologies, making it relevant to the "Saudi Arabia Automotive Sensors Market." I will ensure to frame it as relevant to the market.

Key Market Players

- Bosch KSA

- Continental KSA

- Denso KSA

- Honeywell KSA

- Infineon KSA

- NXP Semiconductors KSA

- Sensata KSA

- TE Connectivity KSA

- Valeo KSA

- Delphi KSA

|

By Vehicle Type

|

By Sensor Type

|

By Application

|

By Region

|

- Passenger Car

- Commercial Vehicle

|

- Temperature Sensor

- Pressure Sensor

- Oxygen Sensor

- Position Sensor

- Motion Sensor

- Torque Sensor

- Optical Sensor

- Others

|

- ADAS

- Chassis

- Powertrain

- Others

|

- Eastern

- Northern & Central

- Western

- Southern

|

Report Scope:

In this report, the Saudi Arabia Automotive Sensors Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Saudi Arabia Automotive Sensors Market, By Vehicle Type:

-

Passenger Car

-

Commercial Vehicle

-

Saudi Arabia Automotive Sensors Market, By Sensor Type:

-

Temperature Sensor

-

Pressure Sensor

-

Oxygen Sensor

-

Position Sensor

-

Motion Sensor

-

Torque Sensor

-

Optical Sensor

-

Others

-

Saudi Arabia Automotive Sensors Market, By Application:

-

ADAS

-

Chassis

-

Powertrain

-

Others

-

Saudi Arabia Automotive Sensors Market, By Region:

-

Eastern

-

Northern & Central

-

Western

-

Southern

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Saudi Arabia Automotive Sensors Market.

Available Customizations:

Saudi Arabia Automotive Sensors Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Saudi Arabia Automotive Sensors Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com