|

Forecast

Period

|

2026-2030

|

|

Market

Size (2024)

|

USD

5.46 Billion

|

|

Market

Size (2030)

|

USD

6.75 Billion

|

|

CAGR

(2025-2030)

|

3.60%

|

|

Fastest

Growing Segment

|

Coupled

|

|

Largest

Market

|

United

States

|

Market Overview

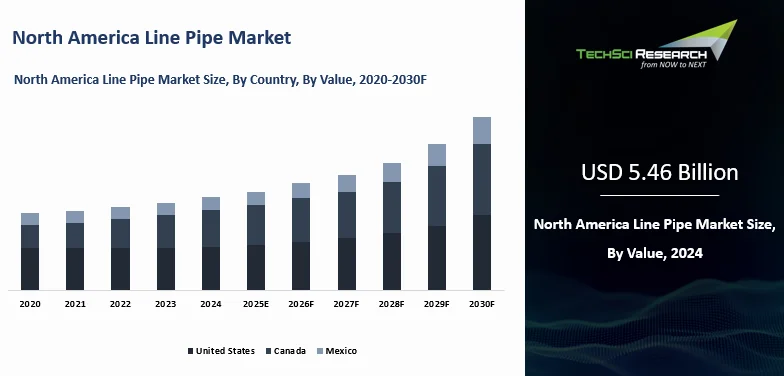

North America Line Pipe Market was valued at USD 5.46 Billion in 2024 and is expected to reach USD 6.75 Billion by 2030 with a CAGR of 3.60% during the forecast period.

The market encompasses the manufacturing, supply, and installation of line pipes used for transporting oil, gas, water, and other fluids across long distances, both onshore and offshore. Typically composed of carbon steel, these pipes are designed to withstand high pressure, corrosive environments, and extreme temperatures. Market growth is driven by rising energy demand, expanding oil and gas exploration, and infrastructure modernization across the United States and Canada. Government support, favorable regulatory frameworks, and increasing LNG and crude oil exports further strengthen demand.

Additionally, the growing adoption of natural gas as a cleaner energy source, advancements in pipe technology, expansion of cross-border energy trade, major pipeline developments, and rising urban and industrial infrastructure needs collectively support sustained market growth.

Download Free Sample Report

Key Market Drivers

Expansion of Oil and Gas Transmission

Infrastructure Across the Continent

The expansion of oil and gas transmission infrastructure remains a core driver of the North America line pipe market because producers and midstream companies continue to add takeaway capacity from major producing regions to refining centers, export terminals, and downstream demand hubs that require long-distance, high-pressure pipeline systems built with high-performance line pipe.

This dynamic is especially important in North America’s integrated energy landscape, where incremental production from Canada and the United States increasingly depends on transmission networks that can move crude oil, natural gas, and related liquids more safely and economically than rail or truck, while also supporting export-oriented growth along the Gulf Coast.

Enbridge’s latest disclosures show how strong this transmission logic remains, with the company describing itself as a leading North American energy infrastructure operator and stating that its Mainline system remained full while delivering an average of over 3 million barrels per day, a clear sign that existing pipe networks are being heavily utilized and still need expansion and optimization. The same pattern is visible in gas transmission, where new pipeline additions are increasingly tied to LNG and industrial demand rather than only domestic heating markets, pushing the industry toward larger and more technically advanced line pipe requirements.

For instance, Enbridge said it sanctioned Mainline Optimization Phase 1 in 2025 for about 1.4 billion US dollars to add 150 thousand barrels per day of Mainline capacity and 100 thousand barrels per day on the Flanagan South Pipeline, while its Rio Bravo and Bay Runner related developments are expected to serve up to 5.3 billion cubic feet per day of natural gas demand for the Rio Grande LNG project, underscoring how major transmission investments continue to create direct and sizable demand for line pipe across North America.

Government-Supported Infrastructure Modernization

Initiatives

Government-backed infrastructure modernization is also a major support pillar for the North America line pipe market because aging water, wastewater, and stormwater systems across the United States are being upgraded through public funding programs that require durable pipe materials with long service life, high corrosion resistance, and stronger compliance with modern safety and environmental standards.

The clearest signal comes from the U.S. Environmental Protection Agency, which says the Infrastructure Investment and Jobs Act delivers more than 50 billion dollars to improve the nation’s drinking water, wastewater, and stormwater infrastructure, marking the single largest federal investment in water infrastructure ever made in the country.

That funding is highly relevant to line pipe demand because it includes 11.7 billion dollars for the Drinking Water State Revolving Fund, 15 billion dollars for lead service line replacement, 11.7 billion dollars for the Clean Water State Revolving Fund, and another 1 billion dollars for clean water emerging contaminants work, all of which point to a broad replacement and reinforcement cycle across underground utility networks. Large private utilities are aligning their own capital programs with this modernization wave, showing that public spending is being reinforced by sustained corporate investment in system renewal rather than acting alone.

For instance, American Water stated in its 2024 annual report that it plans to invest 40 billion dollars to 42 billion dollars over the next decade, with the majority of that capital dedicated to basic replacement of aging pipes and broader upgrades to water and wastewater systems, which highlights how government funding and utility-led reinvestment are working together to sustain demand for line pipes in North American infrastructure renewal.

Urbanization and Industrialization Driving

Municipal Pipeline Projects

Urban growth and industrial expansion are increasingly shaping municipal pipeline demand in North America because growing communities and industrial corridors require more dependable water delivery, wastewater handling, drainage capacity, and utility resilience than legacy networks were designed to provide. In practical terms, this means line pipes are no longer tied only to oil and gas transmission, but also to essential public works that support housing growth, commercial redevelopment, industrial facilities, and stricter environmental management across urban systems.

The infrastructure gap remains substantial, with the EPA stating that the nation has underinvested in water infrastructure for too long and that insufficient systems threaten public health, jobs, and long-term prosperity, which explains why municipal upgrades are becoming a more visible source of pipe demand across the region. Utility operators are responding with larger multiyear replacement programs that focus on buried assets, treatment connections, and network reliability, especially in areas where population density and service expectations continue to rise.

American Water’s operating footprint illustrates the scale of this municipal need, as the company says it serves approximately 1,700 communities and manages pipeline infrastructure totaling 54,500 miles, giving a clear sense of how extensive urban and suburban utility networks already are before further growth and redevelopment are added. For instance, American Water said it expects to invest about 19 billion dollars to 20 billion dollars over the next five years to replace aging infrastructure, upgrade existing or build new facilities, ensure fire protection, and comply with the latest water quality standards, showing how municipal and utility modernization tied to urbanization is becoming an important line pipe demand driver well beyond the energy sector in North America.

Cross-Border Energy Trade Enhancing Line Pipe

Demand

Cross-border energy trade is another important driver of the North America line pipe market because the region’s energy system increasingly relies on pipelines to move Canadian crude into U.S. refining markets and U.S. natural gas into Mexico’s power and industrial sectors, creating sustained demand for high-capacity transmission infrastructure across multiple corridors. This trade pattern strengthens line pipe demand not just through new greenfield projects but also through debottlenecking, looping, compressor additions, and replacement work on existing systems that must handle higher volumes and more complex commercial flows over time.

The Mexico corridor is a particularly strong example, with the U.S. Energy Information Administration reporting that U.S. natural gas pipeline exports to Mexico averaged 6.4 billion cubic feet per day in 2024, up 25 percent from 2019 and the highest annual average on record, while monthly exports reached a record 7.5 billion cubic feet per day in May 2025. The underlying infrastructure still has room to deepen, since the same EIA analysis notes that the four main export corridors to Mexico have a combined capacity of about 14.8 billion cubic feet per day and an approximate utilization rate of 43 percent in 2024, indicating ongoing headroom for future pipeline-linked growth.

For instance, Enbridge said in 2025 that its Mainline Optimization Phase 1 project would increase deliveries of Canadian heavy oil to key refining markets in the U.S. Midwest and Gulf Coast by adding 150 thousand barrels per day on the Mainline and 100 thousand barrels per day on the Flanagan South system under long-term take-or-pay contracts, illustrating how cross-border crude and gas trade continues to translate directly into fresh and sustained line pipe demand across North America.

Key Market Challenges

Rising Regulatory and Environmental Compliance

Pressures

The North America Line Pipe Market is increasingly influenced by stringent regulatory frameworks and heightened environmental scrutiny, creating both operational and financial challenges for industry participants. Growing concerns over environmental risks such as oil spills, methane emissions, and groundwater contamination have prompted authorities across the United States, Canada, and Mexico to enforce stricter compliance standards. Regulatory bodies now mandate frequent inspections, advanced leak detection systems, and comprehensive safety reporting, significantly increasing operational complexity. While these measures are essential for environmental protection and public safety, they often lead to project delays, higher capital expenditure, and prolonged approval timelines for new pipeline developments.

Moreover, compliance requirements extend beyond operations to manufacturing and material sourcing. Companies must adopt sustainable production techniques, low-emission processes, and corrosion-resistant materials that meet evolving environmental benchmarks. This shift demands substantial investment in innovation and workforce training. Additionally, increasing opposition from environmental groups has led to project cancellations and legal challenges, further restraining market growth and short-term profitability.

Volatility in Steel Prices and Raw Material Supply

Chains

Fluctuations in steel prices and disruptions in raw material supply chains pose a significant challenge to the North America Line Pipe Market. Line pipes are primarily manufactured from carbon steel, stainless steel, and specialized alloys, all of which are highly sensitive to global price volatility. Factors such as geopolitical tensions, trade disputes, and economic uncertainties frequently disrupt the supply of essential raw materials like iron ore, coking coal, and ferroalloys. These disruptions result in unpredictable cost structures, making it difficult for manufacturers to maintain stable pricing and profitability. Since pipeline projects are long-term and capital intensive, sudden increases in material costs can delay execution and impact overall project viability.

In addition, supply chain inefficiencies have intensified in recent years due to port congestion, transportation bottlenecks, and limited production capacities. Trade restrictions and tariffs on imported steel further constrain supply availability. As a result, manufacturers must either absorb rising costs or pass them on, affecting competitiveness and limiting investment confidence.

Aging Infrastructure and Rising Maintenance Burden

Aging pipeline infrastructure across North America represents a critical challenge for the line pipe market, increasing both operational risks and financial strain on industry players. Many existing pipelines, originally installed decades ago, are now operating beyond their intended lifespan and are more susceptible to corrosion, structural degradation, and failures. These issues lead to frequent leaks, safety incidents, and service disruptions, necessitating continuous monitoring and maintenance. However, replacing outdated pipelines is a complex and capital-intensive process, often involving regulatory approvals, environmental considerations, and logistical constraints in densely populated or ecologically sensitive areas.

As a result, operators frequently prioritize short-term maintenance and repair activities over full system replacements. This reactive approach diverts investment away from new pipeline projects, limiting market expansion opportunities. Additionally, integrating modern line pipe technologies into legacy systems requires specialized engineering and skilled labor, both of which are in limited supply, further increasing costs and implementation challenges.

Key Market Trends

Integration of Smart Monitoring and Diagnostic

Technologies

The integration of smart monitoring and diagnostic technologies is becoming one of the clearest trends in the North America line pipe market because major pipeline operators are under pressure to manage aging assets more safely, comply with tighter environmental scrutiny, and improve operational visibility across long-distance systems that transport large volumes of crude oil and natural gas every day, which is why tools such as advanced leak detection, inline inspection, AI-assisted analytics, fiber-based sensing, and predictive asset management are moving from optional upgrades to core infrastructure practices across the United States and Canada.

This shift is being reinforced by regulation as well as operator behavior, since PHMSA’s January 2025 final rule on gas pipeline leak detection and repair introduced operator-established Advanced Leak Detection Programs and strengthened the case for more technology-enabled monitoring, while Enbridge says it continues to leverage artificial intelligence to advance safety, emissions reduction, and asset optimization across its network, showing that digital oversight is now being treated as a practical requirement for reliability rather than a future concept.

For instance, Enbridge reported that Mainline volumes averaged 3.1 million barrels per day in 2025 and that the system was apportioned for nine months of the year, a throughput level that helps explain why large North American operators are increasingly pairing high-volume pipe systems with AI-supported optimization and modern diagnostic programs designed to detect anomalies earlier, reduce unplanned downtime, and keep critical transmission assets running within stricter safety and environmental expectations.

Growing Preference for High-Strength,

Corrosion-Resistant Materials

The preference for high-strength and corrosion-resistant materials is also becoming more pronounced in the North America line pipe market because pipeline projects are increasingly expected to operate in harsher service conditions that include high pressure, variable temperatures, corrosive fluids, offshore exposure, difficult soil conditions, and longer operating lives, all of which make conventional pipe less attractive when compared with advanced steel grades, specialized coatings, and higher-performance material systems that can reduce lifecycle risk even if they raise upfront costs.

This change is not just theoretical, as major suppliers are actively positioning their portfolios around performance in corrosive and demanding environments, with Tenaris stating that its onshore line pipe is intended for corrosive environments, low and high temperatures, and high pressure applications, while its offshore portfolio notes that more than 30,000 kilometers of its pipelines have been installed in stringent environments worldwide, reflecting how the competitive edge is increasingly moving toward metallurgical capability, testing, and coating quality rather than simply tonnage.

For instance, Nucor Tubular Products says it operates seven locations across the United States with total capacity exceeding 1.1 million tons per year, while Tenaris says it offers proprietary steel grades for sour and corrosive environments and has qualified seamless and UOE LSAW pipes up to X70 grade for hydrogen transportation at up to 200 bar, illustrating how North American buyers are rewarding suppliers that can combine scale with material durability, corrosion control, and application-specific performance.

Shift Toward Hydrogen and Carbon Capture Pipeline

Infrastructure

The transition to cleaner energy sources is

generating new opportunities within the North America Line Pipe Market,

particularly with the rise of hydrogen fuel and carbon capture and storage

infrastructure. Governments and industries across the region are investing

heavily in decarbonization strategies that rely on transporting hydrogen and

captured carbon dioxide through pipelines over long distances to storage or

conversion sites. This shift is creating demand for a new category of line

pipes specifically engineered to handle the unique chemical properties and

pressure requirements of hydrogen and carbon dioxide.

Unlike traditional oil and gas pipelines, these

emerging pipelines must prevent permeability, embrittlement, and other risks

associated with these gases, requiring specialized materials and welding

techniques. Pilot projects across the United States and Canada are already

underway, signaling a growing commitment to building a dedicated clean energy

pipeline network. Moreover, policy incentives and funding support under clean

energy acts and carbon reduction frameworks are accelerating the timeline for these

projects. As a result, line pipe manufacturers are expanding their product

portfolios and research capabilities to accommodate this evolving demand. This

trend represents a paradigm shift in the North America Line Pipe Market, where

sustainability-driven pipeline projects are beginning to complement and

potentially rival traditional fossil fuel applications.

Segmental Insights

Material Insights

In 2024, the Carbon Steel

segment emerged as the dominant material type in the North America Line Pipe

Market and is expected to maintain its leading position throughout the forecast

period. This dominance is largely attributed to the material’s exceptional

balance between cost-effectiveness, mechanical strength, and wide-ranging

applicability across various pipeline projects, including oil, natural gas, and

water transportation. Carbon steel line pipes have become the preferred choice

for pipeline infrastructure due to their superior tensile strength, ease of

fabrication, and adaptability to high-pressure and high-temperature

environments.

Their compatibility with

welding and forming processes, coupled with an extensive supply chain across

the United States, Canada, and Mexico, has facilitated mass production and

swift deployment in large-scale pipeline networks. The abundance of domestic

raw material sources for carbon steel and the established manufacturing base in

North America have enabled suppliers to offer competitively priced products,

further enhancing the segment’s attractiveness among project developers and

energy companies. Furthermore, carbon steel pipes continue to see innovation

through protective coatings and linings that enhance corrosion resistance and

service life, enabling them to compete effectively even in corrosive

environments where alloy and stainless steel were traditionally preferred.

While other materials like

alloy steel and stainless steel are gaining relevance in niche applications due

to their superior resistance to corrosion and specialized performance, they

often come with significantly higher costs and are primarily used in high-risk

or technically demanding projects. Thermoplastic pipes, although advantageous

for certain low-pressure applications, lack the structural strength required

for large-scale energy pipelines. As demand continues to rise for energy

transportation infrastructure across urban, rural, and cross-border regions,

the carbon steel segment’s dominance is expected to be reinforced by its

reliability, cost efficiency, and adaptability, positioning it as the backbone

of the North America Line Pipe Market well into the future.

Application Insights

In 2024, the Oil & Gas

segment dominated the North America Line Pipe Market and is projected to

maintain its leading position throughout the forecast period. This dominance is

driven by the extensive demand for new and replacement pipeline infrastructure

supporting exploration, extraction, and distribution of oil and natural gas

across the United States, Canada, and Mexico. The segment benefits from

substantial investment in upstream and midstream projects, including

transmission pipelines, gathering systems, and inter-regional connectivity

initiatives.

Rising energy consumption,

cross-border pipeline expansions, and the shift toward cleaner-burning natural

gas are reinforcing the need for durable and high-capacity line pipe systems.

Given the scale and critical importance of oil and gas operations in North

America, this segment is expected to retain its commanding share in the line

pipe market landscape.

Download Free Sample Report

Country Insights

Largest Country

In 2024, the United States emerged as the dominant

country in the North America Line Pipe Market, driven by its expansive energy

infrastructure, ongoing pipeline construction activities, and robust industrial

base. The country has long been at the forefront of oil and gas production, and

the need to transport these resources across vast distances has consistently

fueled demand for durable and cost-efficient line pipes. A surge in shale gas

and crude oil production in regions such as the Permian Basin, Bakken, and

Marcellus has significantly boosted the deployment of new pipeline networks to

support upstream and midstream operations.

In addition, large-scale infrastructure

modernization efforts across water, wastewater, and utility sectors have

further reinforced the use of line pipes in both urban and rural areas. The

United States benefits from a well-established network of pipe manufacturers,

steel suppliers, and engineering contractors, allowing for streamlined supply

chains and competitive pricing. Regulatory emphasis on pipeline safety,

efficiency, and environmental compliance has also driven the adoption of

advanced pipe materials and coatings, ensuring long-term performance. As

government and private sector investments continue to pour into energy and

infrastructure development projects, the United States is expected to sustain

its leading role in the North America Line Pipe Market in the coming years.

Emerging Country

Canada is rapidly emerging as a significant country in the North America Line Pipe Market due to its expanding oil and natural gas

projects, increasing infrastructure investments, and growing focus on energy

exports. The country’s vast natural resources and rising production in regions

such as Alberta have accelerated the need for pipeline development to transport

crude oil and natural gas efficiently.

Government-backed initiatives to modernize water

and wastewater systems in urban and remote communities are supporting the

adoption of line pipes across municipal applications. Canadian manufacturers

are also advancing in producing high-strength, corrosion-resistant line pipes

tailored to harsh climatic and geological conditions. With continued investment

and regulatory support, Canada is expected to strengthen its presence in the

North America Line Pipe Market.

Recent Developments

- In August 2025, Welspun Tubular announced a $150 million investment in Arkansas to add a new LSAW line-pipe mill and an advanced coating facility, a major product-capability expansion for the U.S. market. Trade coverage said the project would make Welspun the only U.S. facility able to manufacture line pipe from 6 inches to 56 inches in diameter, broadening supply options not only for oil and gas pipelines but also for LNG export, hydrogen, and carbon capture applications.

- In June 2025, Graebener announced that its U.S. subsidiary had received a major order from Borusan Berg Pipe to provide key technology for LSAW pipe production, directly linking a machinery supplier with one of North America’s established line pipe manufacturers in a noteworthy technology collaboration. The development matters because LSAW pipe is a core product for large-diameter transmission projects, so equipment upgrades at Borusan Berg Pipe point to continued investment in advanced manufacturing capability for the regional line pipe market.

- In August 2025, Borusan secured a $567 million agreement to supply large-diameter line pipe for the Eiger Express natural gas pipeline project in the United States, marking one of the year’s most visible commercial wins in North American line pipe. According to the report, the pipes will be produced at Borusan Berg Pipe’s facilities in Mobile, Alabama, and Panama City, Florida, with deliveries scheduled through 2026, showing how domestic manufacturing assets are being tied to major U.S. gas infrastructure builds.

- In February 2026, Tenaris said it had joined Trion, Mexico’s first ultra-deepwater project, by securing work to provide line pipe and coatings for bends, flowlines, and risers as part of the subsea infrastructure package. The award is significant for the North American line pipe space because it combines product supply with integrated project services under Tenaris’s One Line offering and ties advanced offshore line pipe demand to a landmark energy development in the region.

Key

Market Players

- Tenaris S.A.

- JFE Steel Corporation

- Nippon Steel Corporation

- TMK Group

- EVRAZ plc

- Welspun Corp Limited

- ChelPipe Group

- United States Steel Corporation

|

By Material

|

By Application

|

By Joint Type

|

By Country

|

- Carbon Steel

- Alloy Steel

- Stainless Steel

- Thermoplastic

|

- Oil & Gas

- Water & Wastewater

- Chemicals & Petrochemicals

- Mining

- Power Generation

- Other

|

- Beveled

- Threaded

- Coupled

- Welded

|

- United States

- Canada

- Mexico

|

Report Scope:

In this report, the North America Line Pipe Market

has been segmented into the following categories, in addition to the industry

trends which have also been detailed below:

- North America Line Pipe Market, By

Material:

o Carbon Steel

o Alloy Steel

o Stainless Steel

o Thermoplastic

- North America Line Pipe Market, By

Application:

o Oil & Gas

o Water & Wastewater

o Chemicals &

Petrochemicals

o Mining

o Power Generation

o Other

- North America Line Pipe Market, By

Joint Type:

o Beveled

o Threaded

o Coupled

o Welded

- North America Line Pipe Market, By Country:

o United States

o Canada

o Mexico

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the North

America Line Pipe Market.

Available Customizations:

North America Line Pipe Market report with

the given market data, TechSci Research offers customizations according to a

company's specific needs. The following customization options are available for

the report:

Company Information

- Detailed analysis and profiling of additional

market players (up to five).

North America Line Pipe Market is an upcoming

report to be released soon. If you wish an early delivery of this report or

want to confirm the date of release, please contact us at sales@techsciresearch.com