|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

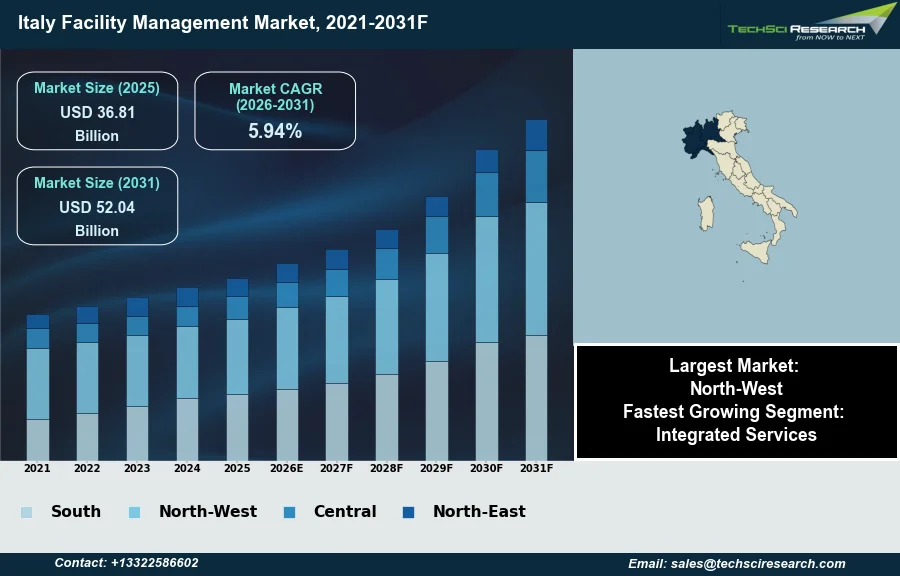

Market Size (2025)

|

USD 36.81 Billion

|

|

CAGR (2026-2031)

|

5.94%

|

|

Fastest Growing Segment

|

Integrated Services

|

|

Largest Market

|

North-West

|

|

Market Size (2031)

|

USD 52.04 Billion

|

Market Overview

The Italy Facility Management Market will grow from USD 36.81 Billion in 2025 to USD 52.04 Billion by 2031 at a 5.94% CAGR. Facility Management (FM) encompasses the integrated management of an organization's buildings, infrastructure, and support services to ensure functionality, comfort, safety, and efficiency for occupants and operations. The Italian Facility Management market is primarily driven by the increasing propensity for outsourcing non-core functions to specialized providers, aiming for enhanced cost efficiency and operational focus. Additionally, the growing emphasis on sustainability and energy efficiency, often spurred by regulatory mandates, alongside advancements in smart building technologies such as IoT and AI, significantly supports market expansion.

Market growth is further evidenced in broader economic indicators. According to Confindustria, salaried employment in its member companies within the services sector, which encompasses facility management, increased by 4.2% between the end of 2023 and the end of 2024. However, a significant challenge impeding market expansion is the intense competition among a multitude of service providers, leading to pricing pressures and potentially reduced profit margins within the sector.

Key Market Drivers

Public Sector Outsourcing and Large-Scale Tenders Driving FM Growth

A significant driving factor within the Italian Facility Management market is the increasing trend of public sector outsourcing initiatives. Government administrations are increasingly delegating non-core functions to specialized external providers to achieve greater efficiency and cost-effectiveness in managing their vast real estate portfolios. This shift is clearly demonstrated by large-scale public tenders. For instance, Consip Spa, the central purchasing body for the Italian Public Administration, published a tender on March 26, 2025, for Facility Management services across large properties and assets used by public administrations, with a substantial base auction amount of €1,428,500,000.00. Such significant procurements underscore the public sector's reliance on private FM firms for operational support, from maintenance to integrated services, thereby fueling market expansion.

Aging Building Stock Drives Modernization and FM Demand

Complementing this, the widespread presence of aging building stock across Italy continues to necessitate modernization and specialized facility management services. A substantial portion of the country's infrastructure requires ongoing maintenance, retrofitting, and energy efficiency upgrades, thereby creating consistent demand for FM providers. For example, the Superbonus measure alone facilitated approximately 500,000 interventions, encompassing 5.8% of Italy's housing stock, by the end of 2024, highlighting the extensive scale of past efforts to address these modernization needs. These deep-seated requirements for upkeep and upgrading older properties ensure a foundational demand for facility management expertise. According to the FIEC Statistical Report, in 2024, the Italian GDP recorded a year-on-year increase of +0.7%, reflecting a general economic environment that supports investment in such services.

Download Free Sample Report

Key Market Challenges

Pricing pressures from market fragmentation threaten margins and growth

The Italian Facility Management market faces significant headwinds from intense competition among a multitude of service providers. This high level of market fragmentation leads to considerable pricing pressures, making it difficult for companies to maintain healthy profit margins and invest in business growth. Service providers frequently prioritize cost-cutting to secure contracts, which can compromise the long-term sustainability and quality of services offered.

Rising labor costs and constrained pricing limit profitability and investment

The impact of these pricing pressures is exacerbated by rising operational expenses. According to a June 2025 agreement for the National Contract for Cleaning Companies, Integrated Services/Multiservices, a significant salary increase of 215 euros at full implementation, representing a 16.6% rise on minimum wage tables, was mandated. Amidst these escalating labor costs, the intense competition within the sector restricts the ability of companies to adequately adjust their service fees. This dynamic contributes directly to reduced profitability and limits the capacity for investment in innovation, technology adoption, and workforce development, thereby impeding overall market expansion.

Key Market Trends

ESG-Driven Compliance and Green Solutions in Facility Management

The Italian Facility Management market is notably influenced by a growing emphasis on ESG compliance and green solutions. This trend extends beyond basic energy efficiency to encompass broader environmental, social, and governance criteria, with regulatory frameworks and corporate sustainability goals driving demand for specialized services. Facility management providers are increasingly tasked with implementing solutions for sustainable operations, waste management, and green building certifications to meet stringent standards. For instance, according to NCA Engineering, October 2025, in "LEED Certification Is Growing Worldwide," 174 projects were certified in Italy in 2024, encompassing over 2.1 million square meters, demonstrating a clear commitment to environmentally sound building practices. This push for compliance and green initiatives reshapes service offerings, requiring expertise in ecological standards and sustainable resource management.

Smart Facility Management Through IoT, AI, and Data Analytics

Another significant trend transforming the market is the digital transformation through smart facility management platforms. This involves the integration of advanced technologies like IoT, AI, and data analytics to optimize building performance, enhance operational efficiency, and provide predictive insights. These platforms move beyond simple automation to enable comprehensive monitoring, remote management, and data-driven decision-making for various facility services. According to Tiesse S.p.A, April 2025, reporting research by the Internet of Things Observatory of the Politecnico di Milano, the Italian Internet of Things market alone reached a value of EUR 9.7 billion in 2024, reflecting a 9% growth compared to the previous year. This highlights the increasing adoption of connected devices and systems that are foundational to smart facility management platforms, allowing for more proactive and efficient facility operations.

Segmental Insights

Integrated Services: Fastest-Growing Segment Driven by Efficiency and Compliance

The Italy Facility Management Market is experiencing a notable trend, with Integrated Services emerging as the fastest-growing segment. This rapid expansion is primarily driven by organizations seeking enhanced operational efficiency and substantial cost optimization through consolidated service provision. Italian businesses and public bodies increasingly prefer a single point of contact for diverse facility needs, which simplifies management and improves service consistency. Furthermore, stringent national regulations regarding safety, energy efficiency, and environmental standards compel companies to adopt comprehensive solutions. Integrated service providers offer the specialized expertise required to navigate these complexities, ensuring compliance and leveraging advanced technologies for streamlined operations and predictive maintenance. This holistic approach resonates with the market's demand for strategic, value-driven facility management.

Regional Insights

North-West Italy: Market Leader in Facility Management

North-West Italy is the leading region in the Italy Facility Management Market due to its robust and diverse economic landscape. This area encompasses significant industrial and financial hubs, including major centers like Milan and Turin, which host concentrations of automotive manufacturing, fashion, technology, and substantial commercial real estate. The advanced economic activity within these sectors generates a high demand for comprehensive facility management solutions to support complex business operations and improve efficiency. Furthermore, the region demonstrates a strong commitment to technological innovation and sustainability, leading to increased adoption of advanced facility management practices that align with stringent economic and environmental regulations. This combination of industrial concentration, economic strength, and progressive operational focus underpins the North-West's market dominance.

Recent Developments

-

In May 2025, SAGAD s.r.l., the Italian subsidiary of B+N Referencia Zrt., completed the acquisition of the facility management operations of L'Alleanza Società Cooperativa, a company based in Verona. This acquisition positioned SAGAD to expand its service portfolio and operational footprint within the Italian facility management sector. The integration of L'Alleanza's facility management activities was intended to enhance SAGAD’s capacity to offer a more diverse and extensive range of services, catering to a broader client base across Italy.

-

In December 2024, Apleona completed the takeover of Galli Facility Management, a move that significantly expanded Apleona's operational presence in Italy. This strategic acquisition was aimed at consolidating Apleona's market share and enhancing its ability to deliver integrated facility management services across various segments within the Italian market. The integration of Galli Facility Management’s expertise and client base was expected to strengthen Apleona's service offerings and reinforce its competitive standing in the Italian facility management industry.

-

In April 2024, Carel Industries inaugurated a new research center at its headquarters located in Brugine, Padua, Italy. This substantial facility spans 4,500 square meters and incorporates advanced climate chambers certified for flammable refrigerants, dedicated testing booths, and an integrated training center. The objective of this investment was to significantly enhance the company's research and development capabilities, particularly within the HVAC sector, which forms a critical component of hard facility management services. This initiative represents a commitment to innovation and technological advancement within the Italian facility management market.

-

In January 2024, ISS, a prominent facility services provider, acquired G.Eco, an Italian facility management company. This strategic acquisition aimed to strengthen ISS's market position within Italy and expand its range of services offered to clients across the country. The integration of G.Eco's operations was expected to enhance ISS's capabilities in delivering comprehensive facility management solutions, reinforcing its presence in a competitive Italian market. This move underscores a trend of consolidation and expansion among key players seeking to optimize service delivery and market reach.

Key Market Players

- Sodexo S.A.

- ISS A/S

- Compass Group plc

- CBRE Group, Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield plc

- ENGIE S.A.

- Cofely Italia S.p.A. (ENGIE Italia)

- Manutencoop Facility Management S.p.A. (now Rekeep S.p.A.)

- Rekeep S.p.A.

|

By Service

|

By Type

|

By Application

|

By Industry

|

By Mode

|

By Region

|

- Property

- Cleaning

- Security

- Catering

- Support and Others

|

|

- Industrial

- Commercial and Residential

|

- Organized and Unorganized

|

|

- South

- North-West

- Central

- North-East

|

Report Scope:

In this report, the Italy Facility Management Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Italy Facility Management Market, By Service:

-

Property

-

Cleaning

-

Security

-

Catering

-

Support and Others

-

Italy Facility Management Market, By Type:

-

Italy Facility Management Market, By Application:

-

Industrial

-

Commercial and Residential

-

Italy Facility Management Market, By Industry:

-

Organized and Unorganized

-

Italy Facility Management Market, By Mode:

-

Italy Facility Management Market, By Region:

-

South

-

North-West

-

Central

-

North-East

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Italy Facility Management Market.

Available Customizations:

Italy Facility Management Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Italy Facility Management Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com