|

Forecast Period

|

2026-2030

|

|

Market Size (2024)

|

USD 1,280.54 Million

|

|

Market Size (2030)

|

USD 2,005.36 Million

|

|

CAGR (2025-2030)

|

7.84%

|

|

Fastest Growing Segment

|

Knee Replacement

|

|

Largest Market

|

South India

|

Market Overview

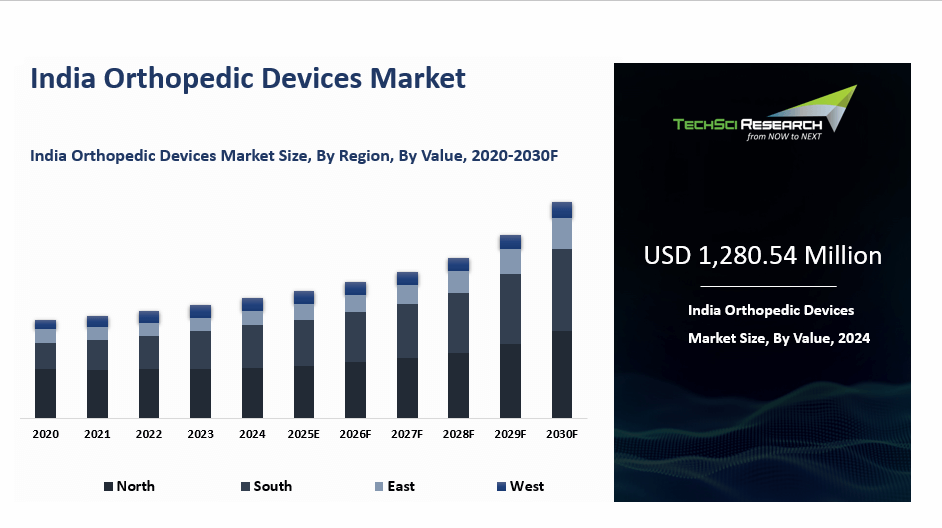

India Orthopedic Devices Market was valued at USD 1,280.54 Million in 2024 and is anticipated to reach USD 2,005.36 Million by 2030, with a CAGR of 7.84% during 2025-2030.

Orthopedic devices are designed to diagnose, manage, and treat musculoskeletal conditions, and are widely used across hospitals, clinics, and surgical centers. They include products such as joint reconstruction systems, braces and supports, trauma fixation devices, spinal implants, prosthetics, and related accessories.

These devices play a vital role in restoring mobility, providing stability, and improving overall quality of life for patients. From joint replacements to supportive braces, they help manage pain, enhance function, and enable patients to maintain active lifestyles.

Continuous advancements in materials and technology, including improved biocompatibility and smart monitoring features, are further enhancing the effectiveness and adoption of orthopedic devices.

Download Free Sample Report

Key Market Drivers

Increasing

Number of Large Joint Reconstruction Surgeries

India is witnessing a strong rise in demand for orthopedic devices as joint reconstruction and replacement procedures become more common, and the available Indian arthroplasty evidence suggests that procedure volumes are already far beyond older estimates, with knee arthroplasty numbers in India estimated at around 200,000 in 2020 and hip arthroplasties expected to grow at one of the fastest rates globally during the first half of the decade.

This momentum is being driven by a growing population entering its 50s and 60s, a very high burden of osteoarthritis, and wider treatment access supported by insurance coverage, government schemes, and price controls that have made surgery more reachable for patients who previously delayed care. Lifestyle-linked obesity, lower physical activity, and joint damage after falls, sports injuries, or earlier trauma are also expanding the pool of patients who eventually require knee or hip reconstruction, which keeps demand elevated for implants, revision systems, and surgical instruments across Indian hospitals.

For instance, the Indian Joint Registry reported that total knee replacements recorded in the registry increased from 1,019 in 2006 to around 27,000 in 2019, and its company-wise analysis showed Johnson and Johnson DePuy accounting for over 35 percent of recorded implant usage while Meril Life Sciences ranked as the second largest supplier, clearly showing how rising surgery volumes are translating into sustained device demand in India.

Growing

Burden of Orthopedic Disorders, Trauma, and Accident Cases

India is seeing rising demand for orthopedic devices because the burden of chronic musculoskeletal disease now overlaps with a very large trauma load from road crashes, workplace injuries, and falls, creating steady need for fracture fixation products, trauma implants, and reconstruction systems across emergency and tertiary care settings.

Road traffic injuries remain especially important in this trend, with a recent review noting that 19 Indians die every hour due to road traffic injuries and that 155,781 road accidents in 2022 were fatal, while the India Status Report on Road Safety highlighted that Uttar Pradesh, Maharashtra, Madhya Pradesh, Karnataka, Rajasthan, and Tamil Nadu together account for nearly half of all road traffic fatalities.

At the same time, an aging population and the spread of obesity and diabetes are increasing osteoarthritis and rheumatoid burden, so more patients now need earlier orthopedic intervention instead of waiting until pain and disability become severe. Better hospital infrastructure, stronger trauma response, and wider awareness of timely treatment are also increasing the number of patients who actually reach facilities equipped for advanced orthopedic care, which supports higher device adoption across both planned and emergency procedures.

For instance, the road safety data highlighted in the India Status Report showed that national highways, despite making up only 2.1 percent of total road length, accounted for 45 deaths per 100 km in 2022, which helps explain why trauma care capacity and demand for fixation and reconstruction devices continue to remain structurally high in India.

Development

of Bioabsorbable and Titanium Implants

India’s orthopedic devices market is also being supported by a clear shift toward more advanced implant materials, with titanium remaining the preferred choice in many joint replacement applications because of its strength, durability, and biocompatibility, while bioabsorbable implants are gaining attention in selected orthopedic uses because they can gradually dissolve and reduce the need for a second removal procedure.

This material transition is highly relevant in India because surgeons and hospitals are looking for solutions that improve stability, lower follow-up burden, and support faster recovery without sharply increasing treatment complexity in a cost-sensitive environment. Growing rates of osteoarthritis, osteoporosis, and trauma injuries are reinforcing this shift, since both elderly joint replacement patients and younger fixation patients benefit from implants that balance mechanical performance with better long-term clinical outcomes. Domestic manufacturing capability is also improving, which matters because India increasingly needs reliable local supply of advanced implants rather than depending only on imported systems for premium procedures.

For instance, CARE Ratings noted that the Meril group was the first company to launch a bioresorbable scaffold in India, while Meril states that its orthopedic portfolio spanning hip, knee, trauma, and spine products is used in more than 50 countries and that its robotic quality checks deliver 0.2 micron accuracy with inspections 30 percent faster than conventional instruments, highlighting how Indian manufacturers are combining absorbable innovation with precision-led titanium and joint replacement platforms.

Increasing

Rate of Geriatric Population

India’s expanding elderly population is becoming one of the most durable demand drivers for orthopedic devices because age is closely associated with osteoarthritis, osteoporosis, fragility fractures, degenerative spine disorders, and reduced mobility, all of which increase the need for implants, assistive devices, and surgical reconstruction.

The demographic shift is large enough to reshape long-term orthopedic demand, as government data projects that the population aged 60 years and above will rise from 100 million in 2011 to 230 million by 2036, meaning nearly one in seven Indians will be an older adult. As this patient base grows, awareness of available treatment options is also improving, and that matters because elderly patients are now more willing to seek intervention for pain, instability, and restricted movement rather than accepting these problems as a normal part of aging. Better access to hospitals, expanding arthroplasty capability, and broader financial support are further strengthening adoption, especially in urban India where specialized orthopedic care is becoming more organized and easier to access.

For instance, the Indian Joint Registry had 712 registered surgeons by June 2020 and found that around 38 percent of reported arthroplasty procedures in the reviewed period were covered by insurance, which signals that treatment capacity and payment support are improving at the same time that India’s elderly population is expanding.

Key Market

Challenges

Poor

Reimbursement Scenario

The

Indian orthopedic device market is currently facing a significant challenge in

terms of poor reimbursement scenarios. Despite the increasing incidence of

orthopedic ailments and accidents necessitating such devices, demand is stifled

due to the high out-of-pocket expenses patients must bear. Moreover, the

current insurance framework in India does not adequately cover the cost of

orthopedic devices, which are often expensive due to the sophisticated

technology involved in their manufacture.

As

a result, many patients are left with limited options and often opt for

cheaper, traditional treatments or even delay necessary procedures. This not

only compromises their health outcomes but also reduces the overall demand for

these devices. Therefore, it is crucial to undertake a comprehensive review and

revision of the insurance reimbursement policies in the healthcare sector,

particularly in relation to orthopedic device coverage. By addressing the issue

of affordability and accessibility of these devices, we can potentially witness

a resurgence in demand and improved health outcomes for patients. This, in

turn, would contribute to the development of a more robust orthopedic device

market in India, fostering innovation and benefiting both patients and industry

stakeholders alike.

Lack

of Skilled Surgeons

The

demand for orthopedic devices in India has experienced a significant downturn

due to a critical shortage of skilled surgeons. This shortage has had a

profound impact on the population, as a substantial portion faces

musculoskeletal conditions such as osteoporosis, arthritis, and trauma injuries

that require orthopedic interventions. However, the lack of qualified

orthopedic surgeons has not only stifled the adoption of these medical devices

but has also resulted in suboptimal usage, further dampening consumer trust and

demand.

The scarcity of proficient surgeons has far-reaching consequences, particularly

in rural areas, where access to orthopedic care is limited. This lack of

accessibility not only hinders the timely treatment of musculoskeletal

conditions but also reduces the overall need for orthopedic devices. It is

worth noting that the deficit of expertise in handling orthopedic devices

raises concerns over the outcomes of surgeries, leading to reluctance amongst

patients to opt for such procedures. Addressing this skill deficit is of utmost

importance to revive the demand for orthopedic devices and to improve

musculoskeletal health in India.

By investing in training and education

programs for orthopedic surgeons, we can ensure that patients receive the

highest quality care and that the utilization of orthopedic devices is

optimized. This, in turn, will not only meet the growing healthcare needs of

the population but also instill confidence in patients and drive the demand for

these life-enhancing medical devices.

Key Market Trends

Alarming

Rise in the Road Accidents

Orthopedic devices in India are experiencing an unprecedented surge in demand, driven primarily by the alarming rise in road accidents, with the country recording 464,029 such incidents in 2023. The increasing number of trauma cases resulting from these accidents, which accounted for 58% of orthopedic trauma cases in one study, often involve severe musculoskeletal injuries, necessitating the use of advanced orthopedic devices for effective treatment and rehabilitation.

As a result, the Indian orthopedic devices market is facing immense pressure to meet this growing need. With road safety remaining a major concern, an average of 20 people died every hour in road accidents in 2023, the number of victims requiring orthopedic support continues to escalate. This includes a diverse range of devices, such as joint implants, screws, plates, and other assistive products, all playing a crucial role in restoring mobility and improving the quality of life for patients.

The country's expanding geriatric population, projected to reach 193.4 million by 2031, is more prone to falls and fractures and further contributes to the demand for orthopedic devices. However, it is the significant surge in road accidents with 29,018 deaths on national highways in just the first half of 2025 that has fundamentally altered the healthcare landscape. This emerging trend underscores the urgent requirement for a robust healthcare infrastructure and increased investment in orthopedic research and development. These efforts are essential to enhance the efficacy of orthopedic treatments and accelerate the recovery process for patients, ultimately leading to improved outcomes and a better quality of life.

Rising

in Health Care Expenditure

India's

healthcare sector has experienced a notable surge in expenditure, driven in

part by the burgeoning middle class that places increased emphasis on health

and wellness. This rise in healthcare spending has had a direct impact on the

demand for orthopedic devices, as more individuals gain access to and can

afford high-quality medical care. The need for orthopedic solutions, ranging

from simple splints and braces to complex joint replacements, has witnessed a

sharp increase.

Moreover, the prevalence of conditions like osteoporosis and

arthritis, combined with an aging population and a rise in lifestyle-related

injuries, further contribute to the growing demand for orthopedic devices.

Technological advancements in the field, such as minimally invasive surgeries

and 3D printing, have also played a pivotal role in driving this demand by

offering improved patient outcomes and treatment options. Consequently, the

escalating healthcare expenditure in India is significantly fueling the growth

of the orthopedic devices market, making it a promising sector with vast

potential for further advancements.

Segmental Insights

Product Type Insights

Based on the product

type, The joint reconstruction segment is expected to maintain its dominance in India’s orthopedic devices market, driven by the growing geriatric population and rising demand for joint replacement procedures to improve mobility and quality of life.

Increasing prevalence of chronic conditions such as diabetes, obesity, osteoarthritis, and osteoporosis is further fueling demand for advanced joint reconstruction solutions.

Additionally, advancements in medical technology and surgical techniques are enabling more personalized and effective treatments, supporting wider adoption. Overall, the segment’s strong growth is driven by aging demographics, disease burden, and continuous innovation in orthopedic care..

Application Insights

Based on application, Knee replacement is the fastest-growing segment in India’s orthopedic devices market, driven by the rising geriatric population and increasing demand for improved mobility and quality of life. More patients are opting for knee replacement procedures to relieve pain and restore function.

Advancements in surgical techniques and materials, including ceramic and titanium implants, along with computer-assisted navigation, are improving outcomes and durability. The growing adoption of minimally invasive procedures is also supporting market growth by enabling faster recovery and reduced complications.

Additionally, increasing awareness and the shift toward personalized treatments, such as customized implants and patient-specific surgical plans, are further boosting the adoption of knee replacement procedures in India.

Download Free Sample Report

Regional Insights

South

India is expected to dominated the Indian Orthopedic Devices Market due to a

combination of factors. The region's rapid urbanization and higher

concentration of healthcare facilities contribute to greater accessibility to

orthopedic devices. With an aging population and lifestyle factors, the South

Indian population exhibits a higher incidence of orthopedic conditions, driving

the demand for these devices. Furthermore, the presence of major market players

in this region not only enhances the availability but also promotes the

adoption of advanced orthopedic devices, further solidifying South India's

position as a key player in the market.

Recent Developments

- In July 2025, Wockhardt Hospitals in Mira Road launched its robotic knee replacement programme with the MISSO robotic system, marking a hospital-level deployment of India’s homegrown orthopedic robotic technology.The hospital said the programme was intended to improve surgical precision and post-operative recovery for orthopedic patients in the Mira-Bhayandar region, showing how domestic robotic devices were moving from demonstration into real clinical adoption.

- In April 2025, MicroPort Orthopedics introduced its second-generation Evolution Medial-Pivot Knee system in India, bringing one of its flagship orthopedic implant platforms into the country. The company said the device was engineered to replicate more natural knee stability and motion through superior flexion stability, anatomic motion, and wear-limiting design, making the launch notable for surgeons and hospitals focused on total knee replacement outcomes.

- In March 2025, Meril’s MISSO, described as India’s first indigenously developed AI-powered robotic system for knee replacement surgery, was showcased during the inauguration of Namo Hospital in Silvassa. The system was presented as a breakthrough in orthopedic robotics because it was designed to improve surgical precision, support faster recovery, and strengthen India’s position in advanced joint-replacement technology with a locally developed platform.

Key Market Players

- Globus Medical India Pvt. Ltd.

- Auxein Medical Pvt. Ltd.

- Smit Medimed Pvt. Ltd.

- GPC Medical Ltd.

- Femur Medical Pvt. Ltd.

- Stryker India Pvt. Ltd.

- India Medtronic Pvt. Ltd.

- Zimmer India Pvt. Ltd.

- Smith+Nephew Healthcare Pvt. Ltd.

- TriMed Solutions (India) Pvt. Ltd.

|

By Product Type

|

By Application

|

By End User

|

By Region

|

|

- Joint Reconstruction

- Spinal Devices

- Orthopedic Braces and Supports

- Trauma Fixation

- Orthopedic Accessories

- Orthopedic Prosthetics

|

- Hip Replacement

- Knee Replacement

- Spine Injuries

- Shoulder Replacement

- Others

|

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers

- Others

|

|

|

|

|

|

|

Report

Scope:

In

this report, the India Orthopedic Devices Market has been segmented into the following

categories, in addition to the industry trends which have also been detailed

below:

- India Orthopedic Devices Market, By Product Type:

o

Joint Reconstruction

o

Spinal Devices

o

Orthopedic Braces and Supports

o

Trauma Fixation

o

Orthopedic Accessories

o

Orthopedic Prosthetics

- India Orthopedic Devices Market, By Application:

o

Hip Replacement

o

Knee Replacement

o

Spine Injuries

o

Shoulder Replacement

o

Others

- India Orthopedic Devices Market, By End User:

o

Hospitals

o

Orthopedic Clinics

o

Ambulatory Surgical Centers

o

Others

- India Orthopedic Devices Market, By Region:

o

North

o

South

o

West

o

East

Competitive

Landscape

Company

Profiles: Detailed

analysis of the major companies present in the India Orthopedic Devices Market.

Available

Customizations:

India

Orthopedic Devices Market report with the given market data, TechSci

Research offers customizations according to a company's specific needs. The

following customization options are available for the report:

Company

Information

- Detailed analysis and profiling of

additional market players (up to five).

India Orthopedic

Devices Market is an upcoming report to be released soon. If you wish an early

delivery of this report or want to confirm the date of release, please contact

us at sales@techsciresearch.com