|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

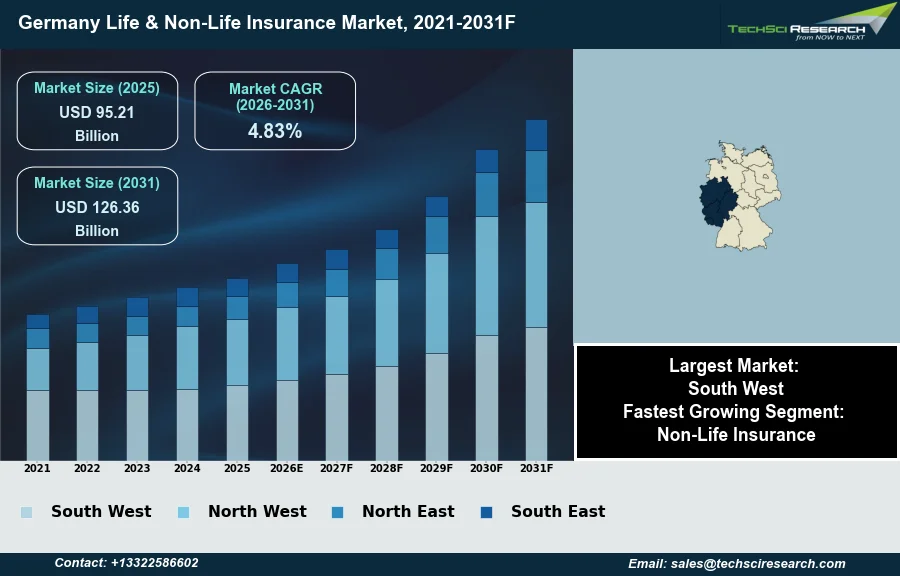

Market Size (2025)

|

USD 95.21 Billion

|

|

CAGR (2026-2031)

|

4.83%

|

|

Fastest Growing Segment

|

Non-Life Insurance

|

|

Largest Market

|

South West

|

|

Market Size (2031)

|

USD 126.36 Billion

|

Market Overview

The Germany Life & Non-Life Insurance Market will grow from USD 95.21 Billion in 2025 to USD 126.36 Billion by 2031 at a 4.83% CAGR. The German Life and Non-Life Insurance market comprises direct gross written premiums derived from policies offering life protection, savings, annuities, motor, property, liability, health supplemental, and accident coverage. Key drivers supporting market growth include Germany's aging demographic, which fuels demand for retirement and long-term financial security solutions, alongside a broader societal emphasis on comprehensive risk management. A stable regulatory framework and heightened consumer awareness regarding insurance benefits also contribute significantly to market expansion. According to the German Insurance Association (GDV), premium income across the sector was projected to grow by 5% in 2025, aiming to reach €250 billion.

Further market support stems from robust household balance sheets and an improving economic outlook, including forecasts for declining inflation and rising real household incomes, which enhance the appeal of insurance products. An increase in the maximum actuarial interest rate for life insurance products, effective January 2025, also positively impacted product attractiveness. Nevertheless, a significant challenge hindering market expansion remains the perceived low value for money in certain products, often attributed to their inherent complexity and persistent high distribution costs.

Key Market Drivers

Aging Demographics Driving Demand in German Insurance

Aging demographics significantly drive demand within the German Life and Non-Life Insurance market, particularly for long-term care, health, and retirement solutions. As the population ages, the need for robust financial provisions against longevity risk and increasing healthcare costs becomes more pronounced. This demographic shift creates a consistent demand for life insurance products that offer secure savings and annuity options, as well as comprehensive health insurance plans tailored for an older demographic. According to the World Bank, in December 2024, the population aged 65 and above in Germany reached 19,372,164 persons, underscoring the expanding base of potential policyholders requiring such specialized coverage.

Digital Transformation Driving Growth in German Insurance

Digitalization and technological innovation further serve as a pivotal growth catalyst by enhancing operational efficiencies and expanding product reach. Insurers are increasingly leveraging digital platforms for improved customer engagement, streamlined policy administration, and sophisticated data analytics for risk assessment and personalized offerings. This technological integration also supports the development of new, flexible insurance solutions that cater to evolving consumer preferences. For instance, according to Allianz SE, in Q3 2023, the company reported a 25% increase in its digital policy sales, demonstrating the tangible impact of digital channels on market penetration. The German insurance industry as a whole reflects this positive trajectory, with total gross written premiums recorded at EUR 238 billion in 2024, according to the Gesamtverband der Deutschen Versicherungswirtschaft, highlighting steady market expansion driven by both demographic needs and digital transformation.

Download Free Sample Report

Key Market Challenges

Low perceived value due to complexity and distribution costs

The perceived low value for money in certain products, often attributed to their inherent complexity and persistent high distribution costs, represents a significant impediment to the growth of the German Life and Non-Life Insurance market.

Perception deters demand and uptake

This perception directly hampers market expansion by deterring potential customers and limiting product uptake. Complex offerings make it difficult for consumers to understand benefits and align them with needs, diminishing perceived worth. This lack of clarity often translates into an unwillingness to commit to new policies or renew existing ones. High distribution costs are frequently passed on, increasing premium prices. This elevation in cost, without a corresponding increase in perceived tangible value, reinforces the notion of poor value for money, making insurance products less attractive. According to the German Insurance Association (GDV), in 2025, total premium income in the German insurance market amounted to €244.5 billion. The combination of product intricacy and high pricing directly curtails consumer demand, thereby restricting overall market development.

Key Market Trends

Rising Adoption of Sustainable Insurance Products and Incentives

Growing adoption of sustainable insurance products represents a pivotal evolution in the German market, driven by increasing environmental consciousness and evolving regulatory landscapes. Insurers are integrating environmental, social, and governance criteria into product development and operational strategies to offer tangible value. This trend fosters innovation in product design, supporting sustainable behaviors and outcomes. According to the GDV Sustainability Report 2025, published in October 2025, the percentage of property and casualty insurers offering policyholders incentives for more sustainable alternatives significantly increased to 62%, from 51% in the previous year. This demonstrates a clear market response to heightened demand for environmentally and socially responsible insurance solutions.

Shift to Proactive Risk Management and Climate-Resilient Claims Management

Concurrently, a significant shift towards proactive risk management and prevention services is reshaping the German insurance landscape. Rather than solely indemnifying losses post-event, insurers are increasingly focusing on mitigating risks before they materialize by providing services that help clients reduce their exposure to potential damages. This involves offering expert advice, implementing preventative technologies, and promoting resilient practices. Such strategies not only aim to reduce claims costs but also enhance customer loyalty. The GDV Sustainability Report 2025, released in October 2025, highlighted that 44% of responding property and casualty insurers are now focusing on climate-resilient solutions in claims management, an increase from 39% in 2024. This strategic realignment emphasizes resilience and foresight in insurance offerings.

Segmental Insights

Non-Life Leads Growth in Germany

The German Life & Non-Life Insurance Market is experiencing notable expansion, with the Non-Life Insurance segment emerging as the fastest growing. This growth is primarily driven by sustained demand for risk protection products amidst an evolving economic landscape. Non-life insurers benefit from positive premium rate adjustments across most segments, which helps to offset increasing claims inflation, particularly in motor and property lines. Furthermore, heightened public awareness of risks from extreme weather events, alongside increased demand for liability and cyber coverage from both retail and commercial clients, is boosting market activity. Regulatory emphasis from the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) on physical climate risk is also encouraging the uptake of comprehensive natural hazard insurance solutions.

Regional Insights

Regional Dominance Driven by Economic Strength

The South West region holds a dominant position within the Germany Life and Non-Life Insurance Market, primarily driven by its robust economic landscape and affluent population. This region, encompassing states like Baden-Württemberg and Hessen, features a high concentration of sophisticated industries such as automotive and mechanical engineering, which generates substantial demand for comprehensive commercial insurance solutions. The elevated disposable incomes of its residents foster a strong propensity for acquiring extensive personal insurance products, including life, health, and property coverage. Furthermore, the stable regulatory framework provided by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin), Germany's integrated financial supervisory authority, underpins market confidence and contributes to the sustained growth and stability observed in the region's insurance sector.

Recent Developments

-

In July 2025, Allianz Commercial launched its Climate Adaptation & Resilience Services (CAReS) platform, a new digital solution for businesses in Germany. This platform was designed to help companies evaluate and mitigate climate risk exposures by converting physical climate risks into financial and physical loss metrics at a portfolio level. Developed in collaboration with clients, CAReS offered consulting expertise and a self-service tool, providing risk scores for twelve environmental perils. This initiative reflected Allianz's commitment to offering innovative non-life insurance solutions that address the increasing challenges of climate change for German businesses.

-

In May 2025, ERGO and Munich Re jointly published the "Tech Trend Radar 2025," providing the insurance industry with an overview of technological innovations and their impact. This report, a collaborative research effort, assessed 36 tech trends, including AI Agents, Spatial Intelligence, and Digital Healthcare, in terms of their maturity and relevance for insurers. The publication offered guidance for German life and non-life insurance companies to understand these drivers and translate their economic implications into business decisions. The initiative highlighted the companies' focus on breakthrough research to navigate the evolving digital landscape of the German insurance market.

-

In August 2024, ERGO, in collaboration with O2 Telefónica and Telefónica Insurance, introduced a new range of embedded insurance products across Germany. This partnership enabled O2's private customers to access supplementary insurance digitally through "O2 Care". The initial offering, "O2 Care | Mobility", launched to provide a mobility guarantee for issues such as rental car breakdowns or bicycle punctures. Customers could book this service for €4.99 per month, with billing integrated into their existing O2 invoice. This initiative marked a strategic move into embedded insurance, integrating coverage directly into third-party products and services within the German non-life insurance market.

-

In January 2024, Allianz Partners unveiled its new allyz mobile application, expanding its digital platform into key European markets, including Germany. This launch provided travelers with a comprehensive digital tool offering trusted advice, expertise, and access to the full suite of Allianz Partners' insurance benefits. The app, developed with technology from Simplesurance, aimed to deliver an intuitive and seamless experience for customers, extending beyond traditional insurance coverage to offer holistic travel support and peace of mind. Its introduction reinforced Allianz Partners' position in digital insurance and assistance services within the German non-life insurance market.

Key Market Players

- Allianz SE

- Münchener Rückversicherungs-Gesellschaft Aktiengesellschaft

- Talanx Aktiengesellschaft

- AXA Konzern AG

- R+V Versicherung AG

- Zurich Gruppe Deutschland

- ERGO Group AG

- HDI Haftpflichtverband der Deutschen Industrie Versicherungsverein auf Gegenseitigkeit

- Debeka Krankenversicherungsverein a. G.

- Generali Deutschland AG

|

By Type

|

By Provider

|

By Region

|

- Life Insurance

- Non-Life Insurance

|

- Direct

- Agency

- Banks

- Others

|

- South-West

- North-West

- North-East

- South-East

|

Report Scope:

In this report, the Germany Life & Non-Life Insurance Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Germany Life & Non-Life Insurance Market, By Type:

-

Life Insurance

-

Non-Life Insurance

-

Germany Life & Non-Life Insurance Market, By Provider:

-

Direct

-

Agency

-

Banks

-

Others

-

Germany Life & Non-Life Insurance Market, By Region:

-

South-West

-

North-West

-

North-East

-

South-East

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Germany Life & Non-Life Insurance Market.

Available Customizations:

Germany Life & Non-Life Insurance Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Germany Life & Non-Life Insurance Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com