|

Key Insights

|

Details

|

|

Forecast Period

|

2027-2031

|

|

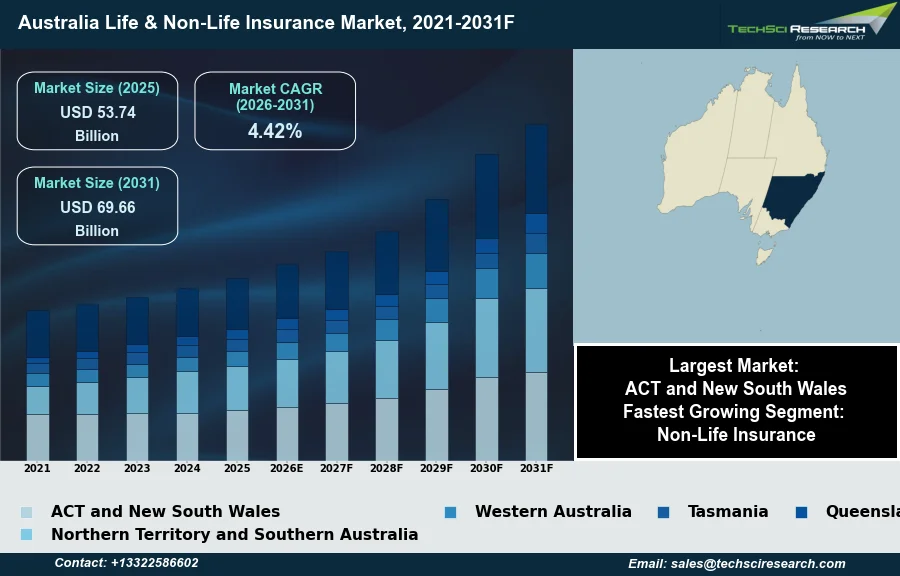

Market Size (2025)

|

USD 53.74 Billion

|

|

CAGR (2026-2031)

|

4.42%

|

|

Fastest Growing Segment

|

Non-Life Insurance

|

|

Largest Market

|

ACT and New South Wales

|

|

Market Size (2031)

|

USD 69.66 Billion

|

Market Overview

The Australia Life & Non-Life Insurance Market will grow from USD 53.74 Billion in 2025 to USD 69.66 Billion by 2031 at a 4.42% CAGR. The Australia Life and Non-Life Insurance Market encompasses all gross premiums written by licensed insurers for life risk, property, motor, liability, health, and other general lines for resident policyholders. Key growth drivers for this market include increasing consumer awareness regarding financial protection and risk management, a stable regulatory framework, demographic shifts such as an aging population, and robust economic growth contributing to higher disposable incomes. According to the Council of Australian Life Insurers, in 2024, life insurers paid out $13.3 billion in claims, reflecting 95 percent of claims submitted.

A significant challenge impeding market expansion is the escalating cost and inherent unpredictability of natural catastrophe events, which directly impact premium affordability and underwriting risks. This is particularly evident in the general insurance segment, where the financial burden from such events is substantial. According to the Insurance Council of Australia, in 2025, Australia's insurers incurred almost $3.5 billion in extreme weather losses, stemming from 264,000 claims.

Key Market Drivers

Digital Transformation and AI Adoption in Australian Insurance

Accelerated Digital Transformation and AI Adoption is profoundly reshaping the Australia Life & Non-Life Insurance Market by optimizing operational efficiencies, enhancing customer engagement, and enabling sophisticated risk assessment. The integration of advanced analytics and artificial intelligence allows insurers to develop highly personalized products and streamline claims processes, catering to evolving consumer expectations for speed and customization. For instance, according to an August 2023 iTnews report, IAG invested $37 million in its digital initiatives during the 2022-2023 financial year, signaling a clear industry trend towards leveraging digital capabilities for competitive advantage and improved service delivery. This transformation is pivotal for maintaining relevance and achieving sustainable growth in a dynamic market environment.

Aging Demographics Driving Demand for Life and Health Insurance

The demographic shift towards an aging population also serves as a significant driver, creating sustained demand for specialized insurance products tailored to longer lifespans and evolving health needs. This trend particularly impacts the life and health insurance segments, where products such as annuities, long-term care, and tailored retirement solutions are becoming increasingly critical for financial planning. According to a December 2024 AXA XL report, 58% of insurance professionals in Australia are over 45, which highlights the broader demographic shift impacting both the workforce and consumer base. This demographic change, coupled with broader market expansion, underpins a robust industry outlook. Overall, the Australian insurance market continues to demonstrate strength; according to APRA, in March 2024, gross written premiums for general insurers increased by 13.9% to $69.7 billion in the year ended December 2023, reflecting overall market dynamism.

Download Free Sample Report

Key Market Challenges

Rising Catastrophe Costs and Premium Pressure

The escalating cost and inherent unpredictability of natural catastrophe events represent a significant impediment to the growth of the Australia Life & Non-Life Insurance Market. These events directly impact premium affordability for resident policyholders, as insurers are compelled to adjust pricing to reflect increased risk exposures. This challenge is particularly acute within the general insurance segment, where the financial burden from such occurrences is substantial and widespread.

Underwriting Strain and Profitability Pressure from Extreme Weather

The heightened frequency and severity of natural disasters also complicate underwriting processes, leading to more stringent risk assessments and potentially limiting coverage options for properties in high-risk areas. According to the Insurance Council of Australia, in 2025, extreme weather events resulted in approximately $4.8 billion in insured losses, stemming from 294,000 claims, demonstrating a substantial financial impact. Such significant and unpredictable payouts directly strain insurers' profitability and capital reserves, ultimately hindering their capacity for market expansion and innovation, and making insurance less accessible or more expensive for consumers.

Key Market Trends

Expansion of Embedded Insurance in Australia

The expansion of embedded insurance models is significantly impacting the Australia Life & Non-Life Insurance Market by integrating coverage directly into non-insurance products and services. This approach offers a frictionless customer experience, allowing policyholders to acquire relevant protection seamlessly at the point of need. Insurers are leveraging digital platforms and strategic partnerships to reach new customer segments and reduce traditional distribution costs, expanding market penetration. According to Fintech Singapore, May 2024, in "Australia's Embedded Insurance Growth Projected to Outpace Traditional Channels", the embedded insurance market in Australia was estimated at A$2.4 billion in gross written premiums in 2024, underscoring its increasing adoption and market influence.

Mainstreaming ESG in Australian Insurance

The mainstreaming of Environmental, Social, and Governance (ESG) frameworks is profoundly reshaping the Australian insurance market by influencing investment strategies, risk assessment, and corporate accountability. Insurers are increasingly integrating ESG considerations into their operations, driven by stakeholder expectations, evolving regulatory landscapes, and a recognition of long-term sustainability benefits. This includes developing new products that address climate risks and investing in socially responsible initiatives, which can enhance brand reputation and attract conscientious capital. According to the Insurance Council of Australia, December 2024, as reported by Insurance Business in "Australian firms push ahead with emission reporting plans", 85% of Australian insurers have pledged to achieve net-zero emissions by 2050, demonstrating a substantial commitment to sustainability goals across the industry.

Segmental Insights

Non-Life Insurance: Fastest-Growing Segment Fueled by Rising Risk Awareness and Regulatory Confidence

The Australian Life & Non-Life Insurance Market is experiencing robust expansion, with the Non-Life Insurance segment emerging as the fastest-growing. This acceleration is primarily driven by heightened consumer awareness and the demand for comprehensive protection against an evolving risk landscape, including home, auto, and specialty lines such as cyber insurance due to increasing incident frequency and severity. Furthermore, the increasing frequency and severity of natural catastrophic events, like floods and bushfires, significantly boost demand for property-related coverage. Strong regulatory oversight by institutions such as the Australian Prudential Regulation Authority (APRA) also contributes by ensuring market stability and insurer solvency, fostering confidence among policyholders.

Regional Insights

ACT and NSW Lead Australia's Life & Non-Life Insurance Market

The Australian Capital Territory and New South Wales collectively lead the Australia Life & Non-Life Insurance Market due to several key factors. New South Wales, particularly with Sydney as the nation's financial hub, possesses robust financial services infrastructure and high levels of commercial activity. This concentration of economic power translates into substantial property values and a high population density, driving significant demand for diverse insurance products and comprehensive risk coverage solutions. The Australian Capital Territory complements this dominance through government-related insurance requirements and a considerable presence of professional service industries, which necessitate extensive commercial liability coverage. Furthermore, the combined regions exhibit a concentration of insured assets and exposure to natural hazards, further stimulating substantial insurance activity. The State Insurance Regulatory Authority (SIRA) also plays a vital role in New South Wales, setting regulatory priorities for the state's insurance schemes, which contributes to market stability and consumer trust.

Recent Developments

-

In October 2025, the Australian life insurance market saw the introduction of a new product with the launch of Futura Protection. This new retail life insurance brand was specifically established for distribution through insurance brokers. The launch signals an expansion in available life insurance options for consumers seeking coverage via professional intermediaries. The brand's entry into the market aimed to cater to evolving consumer needs and preferences within the broader Australian life insurance landscape, offering additional choices and potentially fostering increased competition among providers.

-

In July 2025, a significant collaboration in the Australian non-life insurance market officially commenced as RAA's 20-year insurance partnership with Allianz Australia came into effect. Under this agreement, Allianz South Australia Insurance Limited assumed the underwriting responsibilities for all of RAA's home and motor insurance policies. RAA retained its role in the marketing and distribution of these insurance products, which continue to be offered under the RAA brand. This strategic alliance aims to deliver enhanced benefits and increased value for RAA's extensive membership base, leveraging Allianz's scale while maintaining local brand recognition.

-

In May 2025, Markel Insurance introduced new Financial Institutions (FI) solutions to the Australian market, expanding its specialty non-life insurance product offerings. These localized solutions were designed with specific wordings to cater to a diverse range of organizations within the financial sector. This launch followed the company's introduction of Commercial Professional Indemnity solutions in 2024, demonstrating Markel's ongoing strategy to roll out targeted and tailored insurance products. The new FI solutions provided specialized coverage for various entities, including private equity funds, credit unions, and FinTech companies.

-

In July 2024, TAL, a prominent life insurer in Australia, entered a three-year collaboration with Microsoft to advance its technological capabilities. This partnership focused on leveraging generative artificial intelligence (AI) to enhance operational efficiency and improve customer experience within the life insurance sector. The initiative represented a strategic investment in breakthrough research and development, aiming to integrate advanced AI-driven solutions into various aspects of the company's operations. The collaboration underscored the growing importance of digital transformation and innovative technology in Australia's competitive insurance market.

Key Market Players

- Allianz Australia Limited

- QBE Insurance Group Limited

- Suncorp Group Limited

- Insurance Australia Group Limited

- Zurich Insurance Group Ltd.

- AIA Group Limited

- TAL Dai-ichi Life Australia Pty Ltd.

- MetLife Inc.

- Chubb Limited

- AXA S.A.

|

By Type

|

By Provider

|

By Region

|

- Life Insurance

- Non-Life Insurance

|

- Direct

- Agency

- Banks

- Others

|

- Australia Capital Territory & New South Wales

- Northern Territory & Southern Australia

- Western Australia

- Queensland

- Victoria & Tasmania

|

Report Scope:

In this report, the Australia Life & Non-Life Insurance Market has been segmented into the following categories, in addition to the industry trends which have also been detailed below:

-

Australia Life & Non-Life Insurance Market, By Type:

-

Life Insurance

-

Non-Life Insurance

-

Australia Life & Non-Life Insurance Market, By Provider:

-

Direct

-

Agency

-

Banks

-

Others

-

Australia Life & Non-Life Insurance Market, By Region:

-

Australia Capital Territory & New South Wales

-

Northern Territory & Southern Australia

-

Western Australia

-

Queensland

-

Victoria & Tasmania

Competitive Landscape

Company Profiles: Detailed analysis of the major companies present in the Australia Life & Non-Life Insurance Market.

Available Customizations:

Australia Life & Non-Life Insurance Market report with the given market data, TechSci Research offers customizations according to a company's specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to five).

Australia Life & Non-Life Insurance Market is an upcoming report to be released soon. If you wish an early delivery of this report or want to confirm the date of release, please contact us at sales@techsciresearch.com